Many UK individuals and small businesses with poor or limited credit face a common dilemma when seeking vehicle finance: should they lease or choose hire purchase? Confusion often arises because both options involve monthly payments for cars or vans, yet they differ significantly in commitment, ownership, and accessibility. This article explains these finance options clearly and practically, helping you understand which flexible vehicle solution best suits your short-term needs and credit situation in 2026. Whether you're self-employed, running a startup, or simply need affordable transport without ownership complications, you'll discover how to make an informed choice.

Table of Contents

- What Are Leasing And Hire Purchase? Definitions And Key Features

- Comparing Leasing And Hire Purchase For Poor Or Limited Credit In The UK

- When To Choose Leasing Or Hire Purchase: Practical Scenarios For UK Individuals And Small Businesses

- Understanding Financial And Tax Implications Of Leasing Versus Hire Purchase In The UK 2026

- Explore Flexible Vehicle Leasing With Flexi Auto Lease

Key takeaways

| Point | Details |

|---|---|

| Leasing offers flexibility | Short-term contracts with lower upfront costs and no ownership commitment make leasing accessible for limited credit applicants. |

| Hire purchase leads to ownership | Full payment results in vehicle ownership, but typically requires longer commitment and higher initial deposits. |

| Credit accessibility differs | Leasing approves up to 88% of bad credit applications whilst hire purchase demands stricter criteria. |

| Financial implications vary | Tax treatment, VAT recovery, and cash flow impact differ significantly between both options for small businesses. |

What are leasing and hire purchase? Definitions and key features

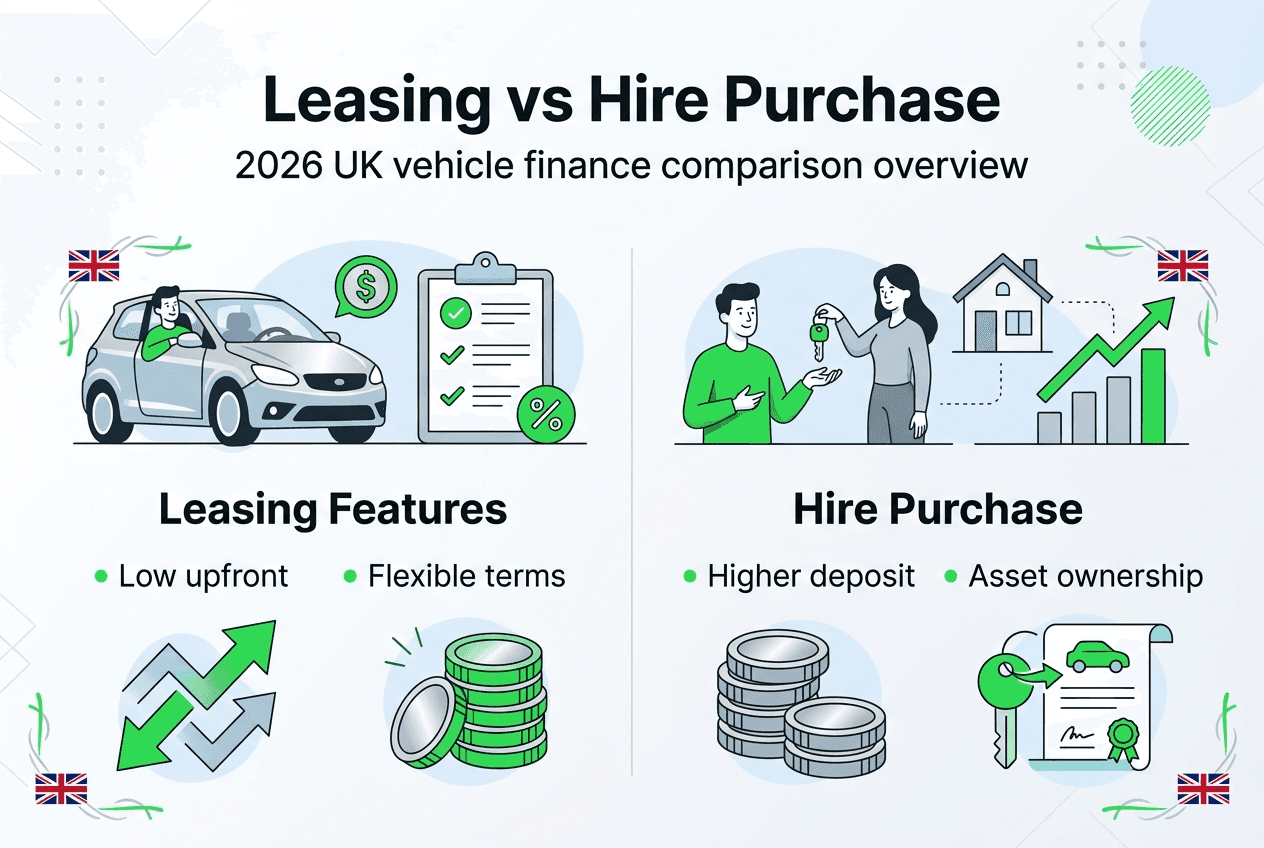

Understanding the fundamental differences between leasing and hire purchase helps you select the right vehicle finance option. Leasing differs from hire purchase in contract terms and ownership rights, making each suitable for different circumstances and credit profiles.

Leasing is a contract-based arrangement where you pay monthly to use a vehicle without ever owning it. Contracts typically run from 6 to 24 months, offering flexibility at the end of your term. You can renew, return the vehicle, or sometimes purchase it at market value. Monthly payments remain predictable, and many agreements include maintenance, road tax, and breakdown cover. This arrangement conserves your cash flow because upfront costs stay minimal compared to purchase options.

Hire purchase represents a finance agreement designed to lead to ownership after you complete all payments. You typically pay an initial deposit, then make fixed monthly instalments over a longer period, often 24 to 60 months. Once you've paid the final instalment, ownership transfers to you. The vehicle serves as security for the loan, meaning the finance company retains legal ownership until full payment. This option suits those who want eventual ownership but cannot afford outright purchase.

Key concepts matter when comparing these options. Monthly instalments vary based on contract length, vehicle value, and your deposit amount. Contract length affects total cost and commitment level. Maintenance responsibilities differ, with leasing often including servicing whilst hire purchase places full responsibility on you. Ownership rights remain with the finance company during hire purchase and never transfer with standard leasing.

Leasing offers several advantages:

- Lower monthly payments compared to hire purchase

- Minimal upfront costs, often just one month's payment

- Flexibility to change vehicles regularly

- Maintenance and servicing often included

- No depreciation worries when returning the vehicle

However, leasing has limitations. You never own the vehicle, mileage restrictions may apply, and early termination can incur fees. Understanding van leasing terminology helps you navigate contracts confidently.

Hire purchase follows a sequential process:

- Choose your vehicle and agree on purchase price

- Pay initial deposit, typically 10% to 20% of vehicle value

- Finance company purchases vehicle and retains legal ownership

- Make fixed monthly payments over agreed term

- Pay optional final fee if required

- Ownership transfers to you after final payment

The leasing process flows differently. You select a vehicle, agree contract terms including length and mileage allowance, then make monthly payments. At contract end, you return the vehicle in good condition, renew for another term, or negotiate purchase if your agreement permits. This flexibility particularly benefits those with changing business needs or uncertain long-term requirements.

Pro Tip: Review contract terms carefully before signing, paying special attention to mileage limits, maintenance obligations, and end-of-contract options to avoid unexpected charges.

Comparing leasing and hire purchase for poor or limited credit in the UK

Your credit history significantly influences which vehicle finance option proves accessible and affordable. Understanding how leasing and hire purchase treat credit applications helps you choose wisely and avoid rejection.

Leasing can offer up to 88% approval rates for bad credit applications in 2026, substantially higher than hire purchase. This difference stems from leasing's non-ownership structure and shorter commitment periods, which reduce lender risk. Finance companies view leasing as lower risk because they retain the vehicle and can repossess it more easily if payments fail.

Hire purchase demands higher deposits and longer terms, creating barriers for people with limited credit. Lenders require larger upfront payments to offset perceived risk, often 20% to 30% of vehicle value. Contract lengths extend to spread costs, but this longer commitment increases total interest paid. Many hire purchase providers conduct hard credit checks that impact your credit score, whilst flexible lease terms accommodate changing financial situations more readily.

| Feature | Leasing | Hire Purchase |

|---|---|---|

| Approval rate for poor credit | Up to 88% | 45% to 60% |

| Typical upfront cost | One month's payment | 20% to 30% deposit |

| Contract flexibility | High, 6 to 24 months | Low, 24 to 60 months |

| Ownership outcome | No ownership | Full ownership after final payment |

| Maintenance responsibility | Often included | Your responsibility |

| Credit check impact | Soft check or none | Hard check affects score |

Leasing advantages for poor or limited credit include:

- Conserves cash flow with lower monthly payments and minimal deposits

- Easier credit approval through flexible assessment criteria

- Option for regular vehicle upgrades without selling or trading

- All-inclusive pricing simplifies budgeting

- Soft credit checks preserve your credit score

- Shorter contracts reduce long-term financial commitment

These benefits make car leasing for bad credit increasingly popular among UK individuals and small businesses facing credit challenges. The ability to drive a reliable vehicle without substantial upfront investment or ownership complications appeals to those rebuilding credit or managing irregular income.

Hire purchase suits different circumstances. If you need eventual ownership for business asset purposes, can afford higher deposits, and prefer fixed costs over longer periods, hire purchase may work despite credit limitations. However, rejection rates remain higher, and failed applications damage credit scores further through hard enquiries.

Pro Tip: Consider your financial situation and vehicle usage needs carefully before choosing, prioritising options that minimise upfront costs and preserve credit score if your history shows limitations.

When to choose leasing or hire purchase: practical scenarios for UK individuals and small businesses

Real-world circumstances determine which vehicle finance option serves you best. These practical scenarios illustrate how your situation, credit profile, and business needs guide your choice.

-

Startup business with limited credit history: New businesses lack trading history and established credit. Leasing suits this scenario because approval criteria focus less on credit scores and more on affordability. Lower upfront costs preserve working capital for business operations. Benefits of short-term leasing include flexibility to upgrade vehicles as your business grows without being locked into long-term commitments that may not suit evolving needs.

-

Seasonal workload fluctuations: Businesses experiencing seasonal demand, such as landscaping or event services, benefit from leasing's flexibility. You can lease additional vans during peak seasons and return them when demand drops, matching vehicle costs to revenue patterns. Hire purchase locks you into permanent ownership and ongoing costs regardless of seasonal changes.

-

Individuals wanting no ownership commitment: If you prefer driving newer vehicles every few years without depreciation concerns or selling hassles, leasing delivers this lifestyle. You avoid maintenance costs, MOT worries, and the burden of disposing of older vehicles. Hire purchase makes sense only if you value ownership and plan to keep the vehicle long-term.

-

Small businesses needing VAT efficiency: VAT-registered businesses can often reclaim VAT on lease payments, improving cash flow. Hire purchase allows VAT recovery on the deposit and finance charges but treats the transaction differently for accounting purposes. Understanding these nuances helps optimise your tax position.

-

Those preferring eventual ownership for asset building: If building business assets matters for balance sheet strength or you want to own the vehicle outright after payments, hire purchase achieves this goal. Ownership provides collateral for future borrowing and eliminates ongoing payments once the contract ends. However, this benefit requires completing a longer commitment and managing higher initial costs.

Choosing between options depends on matching features to your priorities. Car leasing tips for small businesses emphasise assessing your cash flow, credit situation, and vehicle usage patterns. Understanding van leasing vs hire purchase helps commercial users select the right approach for fleet needs.

Your decision should reflect whether you prioritise flexibility over ownership, lower upfront costs over eventual asset value, and shorter commitments over long-term planning. Poor credit applicants typically find leasing more accessible, whilst those with improving credit and desire for ownership may prefer hire purchase despite higher barriers.

Pro Tip: Reassess your vehicle needs regularly to switch to options offering better credit allowances and financial flexibility as your circumstances change.

Understanding financial and tax implications of leasing versus hire purchase in the UK 2026

Financial and tax considerations significantly impact the true cost of vehicle finance, particularly for small business owners managing limited budgets and challenging credit profiles.

Key financial considerations differ between leasing and hire purchase. Monthly costs for leasing typically run lower because you're paying for vehicle use rather than full value. Upfront deposits remain minimal with leasing, often just one month's payment, whilst hire purchase demands substantial deposits. VAT treatment varies, with leasing allowing ongoing VAT recovery on payments for VAT-registered businesses. Ownership asset value matters for hire purchase, as the vehicle becomes a business asset upon full payment, whilst leasing never creates owned assets.

Tax relief differences affect your bottom line. Lease payments may be fully deductible as business expenses, reducing taxable profit immediately. This immediate deduction improves cash flow and lowers tax liability in the current year. Hire purchase allows capital allowances after ownership transfers, spreading tax relief over several years through annual writing down allowances. The timing difference matters when managing fluctuating income or planning tax efficiency.

| Aspect | Leasing | Hire Purchase |

|---|---|---|

| VAT recovery | Reclaim 50% to 100% on payments | Reclaim on deposit and finance charges |

| Tax deduction | Full monthly payment deductible | Interest portion deductible, capital allowances on asset |

| Cash flow impact | Lower monthly costs preserve working capital | Higher deposits and payments strain cash flow |

| Balance sheet treatment | Off-balance sheet, no asset recorded | On-balance sheet once owned, shows as asset and liability |

| Accounting complexity | Simple expense recording | Requires asset depreciation and liability tracking |

Practical impact for businesses managing fluctuating income or poor credit centres on cash flow preservation. Leasing improves small business cash flow by minimising upfront costs and spreading expenses predictably. This predictability helps budget accurately and avoid cash crunches that damage credit further.

Hire purchase offers different advantages. Eventual asset ownership strengthens balance sheets and provides collateral for future borrowing. Capital allowances deliver tax relief, though spread over time rather than immediately. Flexible contract lengths matter less with hire purchase because commitment extends until full payment regardless of changing needs.

Managing financial and tax implications effectively requires:

- Consulting with your accountant about optimal tax treatment for your situation

- Calculating total cost of ownership including interest, deposits, and tax relief

- Assessing cash flow impact of upfront costs versus ongoing payments

- Understanding VAT recovery rules for your business type and vehicle use

- Reviewing balance sheet implications if asset ownership matters for borrowing

- Planning for end-of-contract costs including purchase options or return fees

These considerations prove especially important for businesses with poor credit, where cash flow constraints limit options and every pound matters. Choosing the wrong finance structure can strain budgets, damage credit further through missed payments, or create tax inefficiencies that reduce profitability.

Your individual circumstances dictate which financial and tax profile suits best. Sole traders and small limited companies often prefer leasing's simplicity and immediate tax relief. Larger businesses building asset bases may favour hire purchase despite higher costs and complexity. Understanding these nuances helps you select vehicle finance that supports rather than hinders your financial goals.

Explore flexible vehicle leasing with Flexi Auto Lease

Now that you understand the differences between leasing and hire purchase, finding the right provider makes all the difference. Flexi Auto Lease specialises in flexible car and van leasing across the UK, designed specifically for individuals and small businesses with poor or limited credit history.

They offer short-term contracts from 6 to 24 months with competitive rates and personalised service tailored to your circumstances. Using expert knowledge of the vehicle finance market, their team helps find options that best suit your financial situation and driving needs. Whether you need a commercial van for your startup, a family car despite credit challenges, or seasonal vehicles for fluctuating business demands, they provide accessible solutions with no impact on your credit score. Discover how flexible leasing can work for you at Flexi Auto Lease.

Frequently asked questions

Which option is better with poor credit: leasing or hire purchase?

Leasing generally offers better approval odds and flexibility for poor credit in the UK, with acceptance rates reaching 88% compared to hire purchase's 45% to 60%. Lower upfront costs and soft credit checks make leasing more accessible. However, you should assess your long-term needs and whether eventual ownership matters for your situation.

Can I own the vehicle at the end of a lease?

Most leasing contracts do not offer ownership automatically, as the agreement focuses on vehicle use rather than purchase. Some leases allow you to buy the vehicle at market value when your contract ends, but this option depends on your specific agreement terms. Always clarify end-of-contract options before signing.

How do tax reliefs differ between leasing and hire purchase for small businesses?

Lease payments are usually allowable as a business expense, reducing taxable profit immediately and improving cash flow in the current tax year. Hire purchase allows capital allowances once ownership transfers, spreading tax relief over several years through writing down allowances. The timing and structure of tax benefits differ significantly between both options.

Are there flexible contract lengths available for leasing in 2026?

Yes, leasing contracts in 2026 increasingly offer flexible terms tailored to your needs and credit profile, typically ranging from 6 to 24 months. Flexible contracts help manage changing circumstances, improve affordability through shorter commitments, and allow you to upgrade vehicles as your situation evolves without long-term obligations.