Securing a vehicle lease in the UK can feel impossible when you're stuck between rigid long-term contracts and strict credit checks. Many individuals and small business owners don't realise that flexible contract lengths solve both problems at once. This article reveals why adaptable lease durations offer real advantages for budgeting, credit acceptance, and changing personal or business circumstances in 2026.

Table of Contents

- What Is A Flexible Contract Length In Vehicle Leasing?

- Why Flexible Contract Lengths Matter For Budgeting And Credit

- Comparing Flexible And Fixed-Length Contracts: Pros And Cons

- Who Benefits Most From Flexible Contract Lengths?

- How To Choose A Flexible Contract Length Lease In The UK

- Find Flexible Vehicle Leases Tailored To Your Needs

Key takeaways

| Point | Details |

|---|---|

| Flexible contracts adapt to needs | Lease durations from 1 to 36 months accommodate changing personal or business requirements without long-term commitment. |

| Better approval for bad credit | Short-term leases reduce lender risk, improving acceptance rates for applicants with poor or limited credit history. |

| Budget-friendly customisation | Tailored durations match your cash flow and income patterns, preventing financial overstretch. |

| Easier exit options | Flexible terms allow modifications or early termination with minimal penalties compared to fixed contracts. |

What is a flexible contract length in vehicle leasing?

A flexible contract length lets you choose lease durations that suit your financial situation rather than forcing you into fixed multi-year agreements. Traditional vehicle leases typically lock you in for 24 to 48 months with hefty early termination fees. Flexible lease terms allow customers to choose durations from as short as one month to 36 months or longer, with options to adjust as circumstances change.

These adaptable arrangements offer several practical benefits. You avoid long-term commitment when your job, income, or business needs might shift. Exit options remain straightforward if you need to end the lease early. Most importantly, lenders view shorter terms as lower risk, which matters enormously if your credit history isn't perfect.

Flexible contracts particularly benefit individuals with variable employment, those building credit profiles, and small businesses experiencing seasonal fluctuations. Consider these key features:

- Duration ranges typically span 6 to 24 months with extension options

- Monthly payments adjust based on chosen term length

- Deposit requirements often reduce with shorter commitments

- Approval processes focus less on credit scores and more on current affordability

This flexibility transforms vehicle leasing from an intimidating financial burden into a manageable solution that adapts to your reality.

Why flexible contract lengths matter for budgeting and credit

Short-term and flexible leases fundamentally change how you manage vehicle costs and creditworthiness. Traditional long contracts demand consistent income over years, but flexible contracts reduce financial risk by allowing shorter commitments and potentially lower monthly costs.

Your monthly payment structure benefits immediately. Shorter terms mean you only commit to what you can genuinely afford right now, not what you hope to afford in three years. Deposit requirements typically decrease because lenders face less exposure with brief agreements. This matters enormously when cash flow fluctuates due to self-employment, seasonal work, or recent job changes.

Credit acceptance improves dramatically with flexible durations. Lenders assess shorter leases differently because they're recovering their investment faster. Flexible leasing durations help in budgeting by providing tailored terms that match cash flow and employment changes. Applications that might fail for 36-month contracts succeed with 12-month terms.

Consider these budgeting advantages:

- Align lease payments with seasonal income peaks for small businesses

- Adjust vehicle costs when moving jobs or changing working patterns

- Avoid financial strain from unexpected life changes during long commitments

- Test vehicle suitability before committing to longer agreements

Pro Tip: Review your lease length options every six months when your financial situation changes. This prevents overcommitment and keeps your vehicle costs aligned with current income reality rather than outdated assumptions.

Comparing flexible and fixed-length contracts: pros and cons

Understanding the trade-offs between flexible and fixed contracts helps you make decisions based on your actual circumstances rather than assumptions. Flexible contracts offer greater adaptability and less risk than fixed leases but may sometimes have slightly higher rates to account for that flexibility.

| Feature | Flexible contracts | Fixed-length contracts |

|---|---|---|

| Duration | 1-24 months typically | 24-48 months standard |

| Monthly cost | Potentially higher per month | Often lower per month |

| Deposit | Usually lower | Typically higher |

| Credit requirements | More lenient, bad credit accepted | Strict credit checks |

| Early termination | Minimal penalties, often permitted | Substantial fees apply |

| Total cost | Lower if circumstances change | Better if completed fully |

Flexible contracts shine when your future feels uncertain. Recent job starters, self-employed individuals, and businesses with variable income gain enormous peace of mind from easy exit options. You won't face crushing penalties if circumstances shift unexpectedly. Approval rates soar because lenders view short commitments as manageable risk even with imperfect credit.

Fixed contracts work brilliantly when stability defines your situation. Established employment, predictable income, and confidence in multi-year plans mean you'll likely complete the term. Monthly rates typically run lower because lenders reward long-term commitment. Total costs over the full period often beat flexible alternatives if you actually finish the contract.

Key considerations for your choice:

- Deposit size: Can you afford larger upfront payments for potentially better rates?

- Credit profile: Will strict checks reject your application or merely increase costs?

- Income stability: Does your cash flow support identical payments for years?

- Usage needs: Might your vehicle requirements change with business growth or family circumstances?

Pro Tip: Calculate the total cost including potential early termination fees for fixed contracts. Many people assume fixed deals always cost less, but one early exit penalty often exceeds the entire premium of choosing flexible terms initially.

Who benefits most from flexible contract lengths?

Certain customer profiles gain disproportionate advantages from adaptable lease durations. Understanding whether you fit these profiles clarifies if flexible contracts solve your specific challenges.

-

Individuals with bad or limited credit history face constant rejection from traditional lenders. Flexible short-term leases have up to 88% approval rates for bad credit applicants in 2026. Shorter terms reduce lender risk, transforming impossible applications into approved leases.

-

New job starters and those with recent employment changes struggle to prove income stability over multi-year periods. Individuals with new employment gain approval and budgeting benefits from flexible lease terms because lenders focus on current affordability rather than lengthy employment history.

-

Small businesses with fluctuating cash flow need vehicle costs that scale with income. Seasonal businesses, contractors, and growing enterprises avoid the financial stress of fixed payments during lean months. Flexible terms let you match vehicle expenses to revenue patterns.

-

Self-employed entrepreneurs face unique challenges proving consistent income to traditional lenders. Variable monthly earnings that defeat fixed contract applications work perfectly with short-term flexible arrangements that assess current capacity.

-

Temporary residents or those with uncertain long-term plans avoid committing to leases that extend beyond their UK stay. Flexible durations prevent paying termination penalties when circumstances inevitably change.

The inclusive nature of flexible leasing fundamentally widens mobility access. People previously excluded from vehicle leasing due to credit, employment, or income variables suddenly qualify. This democratisation matters enormously for individuals rebuilding credit, starting businesses, or navigating life transitions.

How to choose a flexible contract length lease in the UK

Selecting the optimal flexible lease requires evaluating providers systematically rather than accepting the first offer. A checklist approach focusing on flexibility, total cost, and credit acceptance criteria helps choose the ideal arrangement.

Follow these steps to secure the best flexible lease:

-

Research providers specialising in flexible terms rather than traditional leasing companies. Specialist providers understand bad credit, variable income, and adaptable needs far better than mainstream lenders focused on perfect credit profiles.

-

Compare quotes from multiple providers, ensuring you understand total costs including any admin fees, delivery charges, or potential adjustment penalties. The lowest monthly payment rarely represents the best overall value.

-

Check contract details meticulously, particularly clauses covering lease modifications, early termination, and extension options. These terms define whether your "flexible" contract actually delivers promised adaptability.

-

Verify credit policies explicitly, asking whether applications involve hard or soft credit checks and how bad credit affects approval or pricing. Transparency here prevents wasted applications and credit score damage.

-

Seek expert advice from providers offering consultative services rather than purely transactional relationships. Experienced advisors suggest optimal durations and structures for your specific circumstances.

-

Review insurance and maintenance inclusions, as all-inclusive packages often deliver better value than separately arranged cover, particularly for short-term leases.

Pro Tip: Ask specifically about no deposit options and the shortest available terms to maximise financial ease. Many providers offer these but don't advertise them prominently, reserving them for customers who enquire directly.

Reading terms prevents nasty surprises. Pay particular attention to mileage limits, vehicle condition requirements, and any charges for modifications or early returns. Understanding these upfront avoids penalties that undermine the flexibility you're paying for.

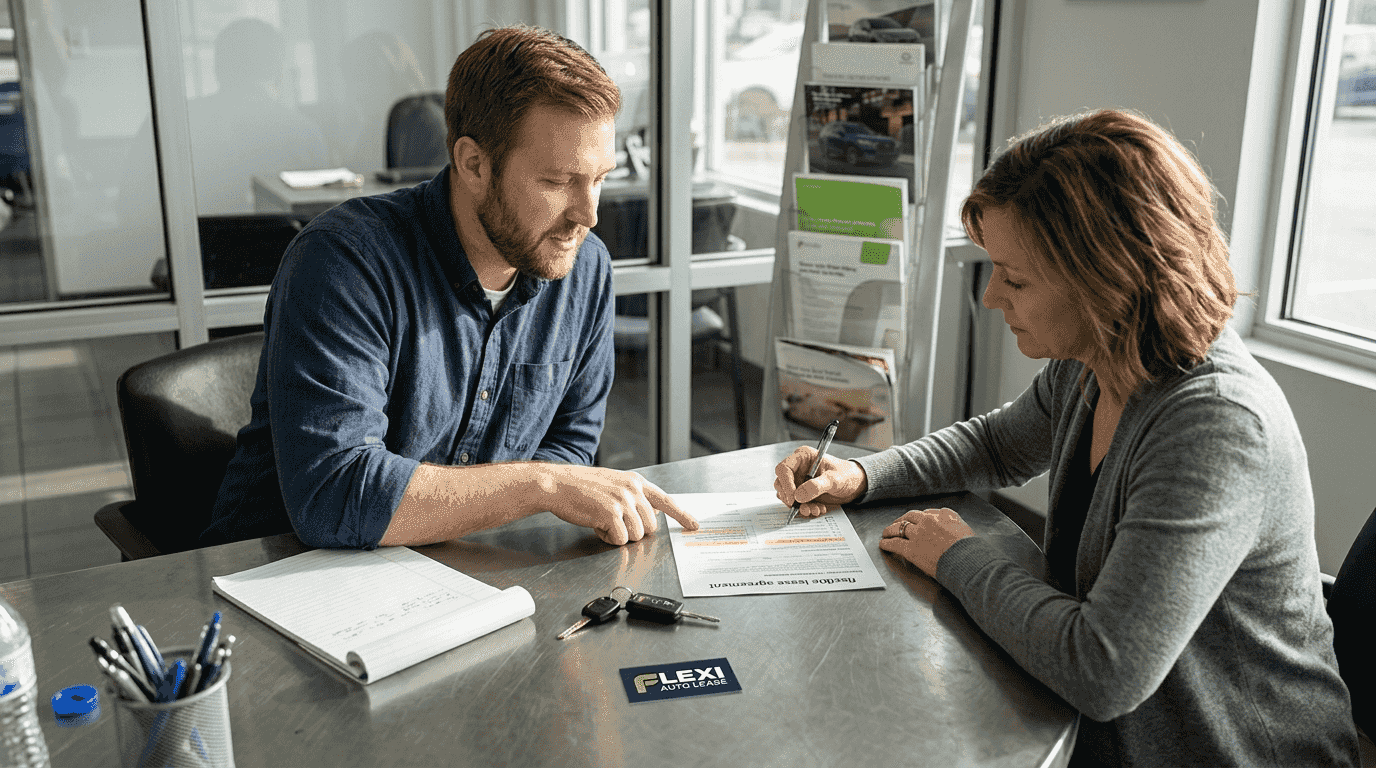

Find flexible vehicle leases tailored to your needs

Navigating the flexible leasing market becomes straightforward when you work with specialists who understand your specific challenges.

Flexi Auto Lease specialises in flexible, short-term vehicle leases across the UK, with particular expertise helping individuals and small businesses overcome credit challenges. Our approval process focuses on current affordability rather than perfect credit history, achieving exceptional acceptance rates even for applicants with bad or limited credit. We offer lease durations from 6 to 24 months with all-inclusive pricing covering road tax and maintenance. Nationwide delivery means your approved vehicle arrives within days. Visit Flexi Auto Lease to explore current offers and discuss bespoke leasing arrangements with our expert team.

FAQ

Can I get a flexible contract lease if I have bad credit?

Absolutely. Flexible short-term leases have up to 88% acceptance in 2026 for applicants with poor credit. Shorter contract durations reduce lender risk substantially, making approval far more likely even with credit challenges. Many flexible lease providers use soft credit checks that don't impact your credit score, focusing instead on current income and affordability.

What happens if I need to change my lease length after signing?

Flexible contracts commonly allow modifications or early terminations with minimal penalties compared to fixed-term leases. Specific terms vary by provider, so review your contract's adjustment clauses before signing. Most flexible arrangements permit extensions easily, whilst early termination typically requires notice periods ranging from 30 to 90 days.

Are flexible leases more expensive than fixed-term ones?

Monthly payments may run slightly higher to cover the added adaptability, but flexible leases often save money overall by avoiding penalties and long commitments. Consider total cost including potential early termination fees from fixed contracts. One penalty charge from ending a fixed lease early often exceeds the entire premium of choosing flexible terms initially.

How short can a flexible vehicle lease be?

Flexible leases typically range from one month to 36 months, with most providers specialising in 6 to 24-month terms. Some specialists offer rolling monthly contracts that continue until you provide notice. Shorter durations suit temporary needs, trial periods, or highly variable circumstances, whilst 12 to 18-month terms balance flexibility with reasonable monthly costs.

Do flexible leases include insurance and maintenance?

Many flexible lease providers offer all-inclusive packages covering road tax, maintenance, and breakdown cover. Insurance typically remains your responsibility unless specifically included in premium packages. All-inclusive options simplify budgeting and often deliver better value than separately arranged services, particularly for short-term leases where administrative overhead otherwise inflates costs disproportionately.