Many people believe poor credit history eliminates car leasing as an option, but that's simply not true in 2026. Short-term vehicle leasing across the UK now offers accessible, flexible solutions specifically designed for individuals and small businesses facing credit challenges. This guide explains how car leasing works, what it costs, and why soft credit checks and all-inclusive pricing make it a practical alternative to traditional car finance for those with bad or limited credit history.

Table of Contents

- Understanding Car Leasing And Its Mechanics

- Leasing Eligibility For Bad Or Limited Credit In The UK

- Financial Terms And All-Inclusive Pricing In Leasing

- Comparison Of Leasing Versus Buying With Credit Constraints

- Practical Benefits For Self-Employed And New Employment Leasers

- Explore Flexible Car Leasing Solutions Today

- Frequently Asked Questions About Car Leasing With Bad Credit

Key takeaways

| Point | Details |

|---|---|

| Flexible access without ownership | Car leasing enables vehicle use on short-term UK contracts (6-24 months) without committing to purchase. |

| Bad credit friendly approval | Soft credit checks and lower upfront costs make leasing accessible for limited or poor credit histories. |

| Simplified budgeting | All-inclusive pricing covers road tax, maintenance, and servicing in one monthly payment. |

| Rapid approval process | Lease applications often complete within days, enabling quick vehicle access for urgent needs. |

| No depreciation risk | Leasing avoids resale value concerns and unexpected repair costs common with ownership. |

Understanding car leasing and its mechanics

Car leasing is fundamentally a rental agreement where you pay monthly to use a vehicle for a fixed period without ever owning it. Unlike buying a car outright or taking out a traditional loan, short-term leasing contract flexibility allows you to drive a reliable vehicle without the financial burden of ownership or long-term commitment.

In the UK, typical lease agreements span 6 to 24 months with predictable monthly payments. You choose your vehicle, agree to terms including mileage limits and maintenance responsibilities, then return the car at the contract's end. This arrangement differs sharply from purchasing, where you take on full ownership costs, depreciation risks, and eventual resale challenges.

The core mechanics are straightforward:

- You select a vehicle based on your needs and budget constraints

- The leasing provider retains ownership whilst you use the vehicle

- Monthly payments cover your usage rights for the agreed period

- Mileage limits prevent excessive wear, with potential fees for overuse

- At contract end, you simply return the vehicle with no resale hassle

Leasing grants immediate vehicle access without committing to full purchase costs or worrying about how market depreciation affects your investment. For those managing credit challenges, this structure proves far more accessible than traditional car finance options that demand substantial deposits and pristine credit scores.

Leasing eligibility for bad or limited credit in the UK

The remarkable advantage of modern car leasing lies in how providers accommodate customers with challenging credit histories. Traditional car finance typically requires hard credit checks that damage your score and often result in rejection for those with poor credit. Leasing with flexible credit checks takes a fundamentally different approach, prioritising soft checks or even forgoing credit checks entirely.

Soft credit checks allow providers to assess your circumstances without impacting your credit score, making approval significantly more achievable for those rebuilding their financial standing. This process recognises that credit scores don't tell the complete story of your ability to meet monthly payment obligations, especially if you're newly employed or recently self-employed.

Key accessibility factors include:

- Soft credit checks preserve your credit score during application

- Providers evaluate current income and affordability rather than past credit mistakes

- Approval timelines often complete within 24-48 hours, not weeks

- No requirement for guarantors or co-signers in many cases

- Lower deposit requirements compared to traditional finance agreements

Pro tip: When applying for a lease with bad credit, gather recent payslips, bank statements, and proof of address beforehand. Demonstrating stable income and current financial responsibility matters more than historic credit issues to flexible leasing providers.

Many UK leasing companies now specialise in serving customers with limited or poor credit, recognising this represents a substantial market of responsible individuals whose credit histories don't reflect their current reliability. This shift has transformed vehicle access for thousands who previously faced rejection from traditional lenders.

Financial terms and all-inclusive pricing in leasing

Understanding exactly what you pay for matters enormously when evaluating leasing affordability. Unlike car ownership where costs scatter across insurance, tax, MOT, servicing, and unexpected repairs, all-inclusive leasing contracts bundle these expenses into one predictable monthly payment.

Typical all-inclusive packages cover:

- Road tax for the entire lease duration

- Scheduled servicing and maintenance at approved centres

- Breakdown cover for emergency roadside assistance

- Replacement tyres when tread depth falls below legal limits

- Minor repairs not resulting from negligence or accidents

This comprehensive approach transforms budgeting from unpredictable to manageable. You know precisely what vehicle costs you'll face each month, eliminating the financial stress of sudden repair bills or forgotten tax renewals that plague many car owners.

Upfront costs remain significantly lower than purchasing alternatives. Where buying a car might demand a £2,000-£5,000 deposit plus first month's payment, leasing often requires just the initial monthly payment or a modest upfront fee of a few hundred pounds. This accessibility proves crucial for those rebuilding finances after credit difficulties.

"All-inclusive leasing removes the guesswork from vehicle costs. You gain reliable transportation without worrying whether you can afford next month's unexpected garage bill or whether you've budgeted enough for the annual service."

One consideration deserves attention: mileage limits. Most contracts specify annual mileage allowances, typically 8,000-15,000 miles. Exceeding these limits incurs per-mile charges, usually 5-15 pence depending on the vehicle. Accurately estimating your driving needs prevents surprise fees when returning the vehicle.

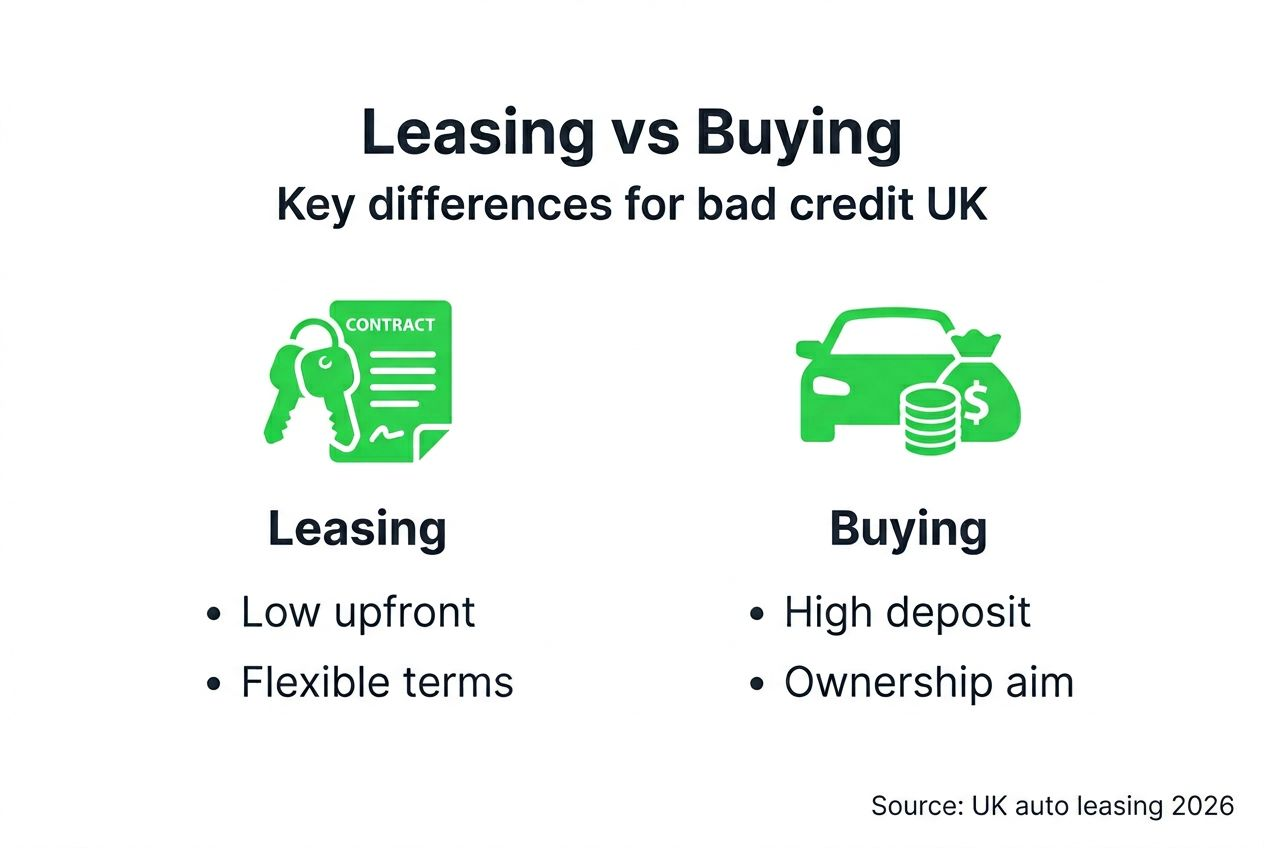

Comparison of leasing versus buying with credit constraints

When credit history limits your options, choosing between leasing and buying requires careful evaluation of your circumstances. Both routes offer vehicle access, but the financial implications differ substantially for those managing credit challenges.

| Factor | Leasing | Buying with finance |

|---|---|---|

| Upfront cost | £200-£500 typical | £2,000-£5,000+ deposit |

| Credit requirements | Soft checks, bad credit accepted | Hard checks, good credit preferred |

| Monthly payments | £200-£600 all-inclusive | £250-£700+ plus separate costs |

| Depreciation risk | None, not your concern | Full risk, affects resale value |

| Maintenance included | Usually yes, fully covered | No, your responsibility |

| Contract flexibility | 6-24 months, easy changes | 3-5 years, difficult to exit |

| Ownership | Never, return at end | Yes, vehicle becomes yours |

Leasing versus buying for credit constraints reveals distinct advantages depending on your priorities. Leasing requires minimal upfront investment, making it achievable for those without substantial savings. Your monthly payment remains fixed and predictable, covering nearly all vehicle costs.

Buying with finance demands higher credit scores and larger deposits, often placing it beyond reach for those with poor credit. Even when approved, higher interest rates for bad credit borrowers substantially increase total costs. You also shoulder full depreciation risk, typically losing 40-60% of the vehicle's value over three years.

Key decision factors:

- Choose leasing if you need flexibility, have limited savings, or face credit challenges

- Consider buying if you drive high mileage, want eventual ownership, or have excellent credit

- Leasing suits short-term needs, frequent vehicle changes, or business use

- Buying makes sense for long-term ownership beyond five years

Pro tip: Calculate total cost over your intended usage period. If you'll keep a vehicle beyond four years and drive modest mileage, buying might cost less overall. For shorter terms or uncertain future needs, leasing typically proves more economical and definitely more accessible with poor credit.

The flexibility advantage cannot be overstated. Life circumstances change, especially for the self-employed or those in new employment. Leasing lets you adjust your vehicle choice every 6-24 months without the hassle of selling and buying repeatedly.

Practical benefits for self-employed and new employment leasers

For individuals establishing businesses, recently employed, or managing fluctuating income, benefits of leasing for self-employed solve multiple challenges simultaneously. Traditional lenders view these situations as high-risk, often declining applications despite strong current income.

Modern leasing providers recognise that recent employment changes or self-employment don't indicate unreliability. They assess your current affordability and income stability rather than demanding years of employment history or perfect credit scores.

Primary advantages include:

- Rapid approval processes completing within 24-72 hours enable immediate vehicle access when you need reliable transport for work

- Fixed all-inclusive costs simplify business accounting and personal budgeting without surprise expenses

- Short-term contracts (6-24 months) match business growth phases without long-term commitment

- Vehicle flexibility allows upgrading or downsizing as your circumstances evolve

- No depreciation concerns mean you avoid losses if your business direction changes

Self-employed individuals particularly benefit from predictable costs. When income fluctuates month to month, knowing exactly what you'll pay for transport removes a significant stress factor. All-inclusive pricing means no unexpected garage bills derailing your monthly budget during lean periods.

For those in new employment, leasing provides immediate transport solutions whilst you establish financial stability. You need a reliable vehicle to maintain employment, but traditional finance remains inaccessible during probation periods. Flexible leasing bridges this gap effectively.

Additional practical benefits:

- Nationwide delivery brings vehicles directly to your door, saving time

- Wide vehicle selection including cars, SUVs, electric vehicles, and commercial vans

- No long-term commitment allows testing whether vehicle ownership suits your lifestyle

- High user satisfaction reflects the real-world reliability and convenience these arrangements provide

The administrative simplicity cannot be overlooked. One monthly payment covers everything, one provider handles all vehicle concerns, and one contract defines your obligations clearly. For busy entrepreneurs and employees focused on career development, this streamlined approach saves valuable time and mental energy.

Explore flexible car leasing solutions today

Now that you understand how car leasing works and why it suits those managing credit challenges, the logical next step is exploring actual leasing options tailored to your circumstances. Whether you need a reliable car for daily commuting, an electric vehicle for environmentally conscious driving, or a commercial van for your growing business, flexible UK car leasing solutions provide accessible choices regardless of your credit history.

You'll discover a straightforward three-step process designed specifically for individuals and small businesses seeking short-term leasing flexibility. Browse diverse vehicle options, submit a simple application with soft credit checking, and potentially drive your chosen vehicle within days. All-inclusive pricing covers road tax, maintenance, and servicing, whilst flexible 6-24 month terms adapt to your evolving needs without long-term financial commitment. Fast approvals and personalised service ensure you gain reliable transportation quickly and affordably, even with bad or limited credit.

Frequently asked questions about car leasing with bad credit

How does bad credit affect my chances of getting a car lease in the UK?

Bad credit impacts traditional finance severely but affects flexible leasing minimally. Providers using soft credit checks focus on your current income and affordability rather than past credit mistakes, making approval significantly more achievable. Many UK leasing companies now specialise in serving customers with poor or limited credit histories specifically.

Can I lease electric or commercial vehicles with limited credit history?

Yes, flexible leasing providers offer diverse vehicle types including electric cars and commercial vans to customers with limited credit. The same soft credit check approach applies regardless of vehicle type, ensuring access to modern, efficient vehicles without the barriers traditional finance imposes. Vehicle choice depends more on your budget and needs than your credit score.

What costs are usually included in an all-inclusive leasing contract?

All-inclusive leasing typically covers road tax, scheduled servicing, routine maintenance, breakdown cover, and replacement tyres when needed. This comprehensive approach bundles most vehicle costs into one predictable monthly payment, eliminating surprise repair bills or forgotten tax renewals. Insurance remains your responsibility, though some providers offer optional insurance packages.

How flexible are short-term leases if my personal or business needs change?

Short-term leases excel at flexibility, with 6-24 month contracts allowing regular vehicle changes as your circumstances evolve. If your needs change mid-contract, many providers offer early termination options or vehicle swaps, though terms vary. This adaptability proves invaluable for self-employed individuals and those in new employment facing uncertain future requirements.

Will leasing a car impact my credit score in the future?

Leasing with soft credit checks does not damage your credit score during application or throughout the contract. Successfully maintaining payments may actually improve your credit over time by demonstrating financial responsibility. Only missed payments would negatively affect your score, making it crucial to choose affordable monthly payments within your reliable budget.