Many people with bad or limited credit assume van leasing is beyond their reach because the terminology feels deliberately complicated. The truth is simpler: understanding just a handful of key terms unlocks flexible leasing options across the UK in 2026. This guide cuts through the jargon to explain essential van leasing terminology, helping you make confident decisions whether you need a vehicle for personal use or your small business. By the end, you'll know exactly what to look for and which questions to ask.

Table of Contents

- Essential Van Leasing Terms You Need To Know

- How Flexible Lease Terms Help Those With Bad Or Limited Credit

- Common Pitfalls In Van Leasing Terminology And How To Avoid Them

- Practical Steps To Apply Your Van Leasing Knowledge In 2026

- Find Flexible Van Leasing Options With Flexi Auto Lease

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Leasing terms impact costs | Understanding mileage allowance, residual value, and contract length prevents unexpected charges and helps you choose the right deal. |

| Credit status affects options | Flexible lease terms and no deposit deals specifically support approval for those with bad or limited credit histories. |

| Contract flexibility matters | Shorter lease periods and early termination clauses provide escape routes if your circumstances change. |

| Terminology empowers decisions | Knowing the difference between leasing and hiring helps you select the most cost-effective solution for your needs. |

| Fine print requires attention | Excess mileage penalties and cancellation fees hide in contracts, so always clarify terms before signing. |

Essential van leasing terms you need to know

Van leasing comes with its own vocabulary, and grasping these core terms transforms confusing offers into clear choices. Leasing means paying monthly to use a vehicle you don't own, with the leasing company retaining ownership throughout the contract. This differs fundamentally from buying or financing, where you eventually own the asset.

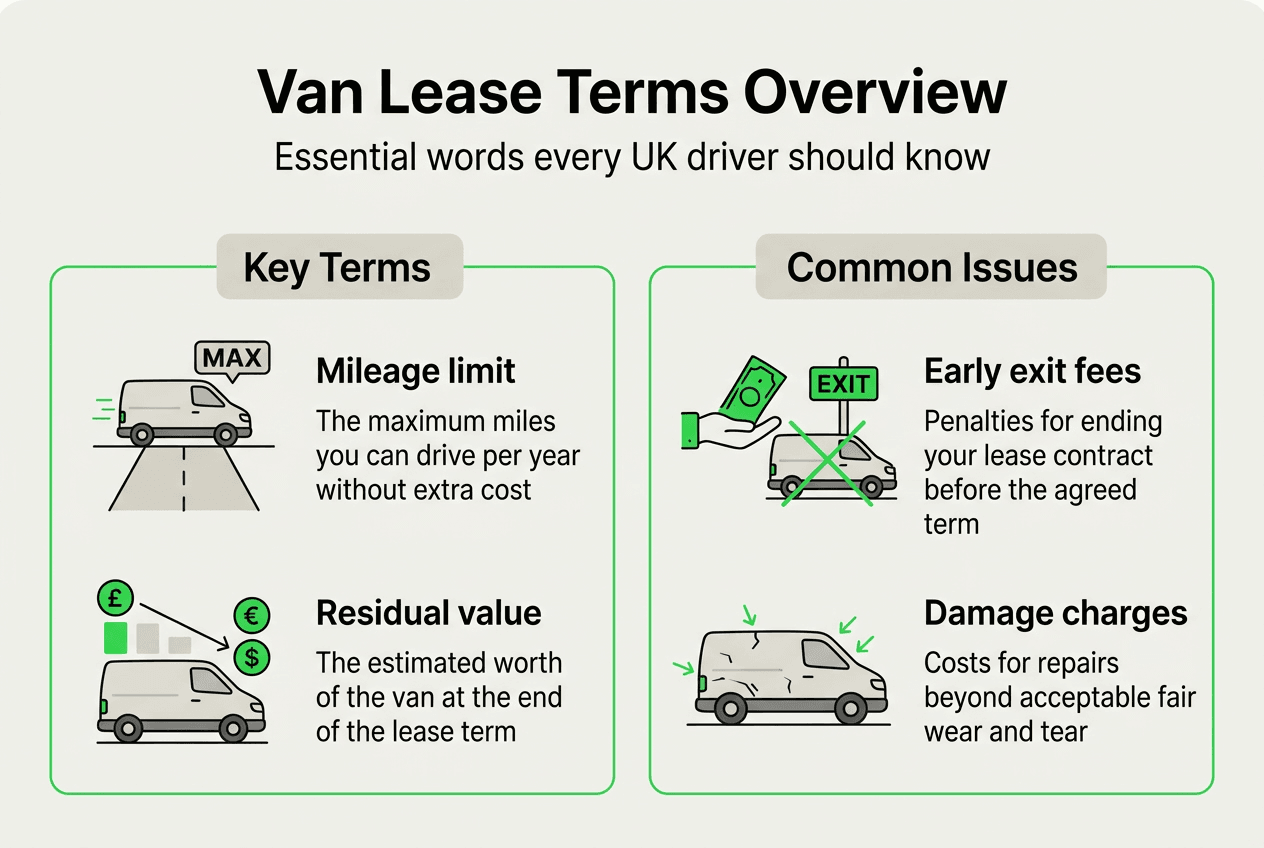

Mileage allowance sets the annual distance you can drive without penalty, typically ranging from 5,000 to 30,000 miles per year. Exceed this limit and you'll face excess mileage charges, often 10p to 25p per mile. Residual value represents what the leasing company expects the van to be worth at contract end, influencing your monthly payments. Higher residual values generally mean lower monthly costs because you're only paying for the vehicle's depreciation during your lease period.

No deposit leasing eliminates upfront payments, making van leasing more accessible for bad credit applicants who lack savings. Instead of paying thousands upfront, you spread costs across monthly payments. This approach particularly benefits small business owners managing tight cash flow or individuals rebuilding their credit profiles.

For those with bad or limited credit, understanding these terms matters even more. Leasing companies assess risk differently than traditional lenders, often focusing on affordability rather than credit scores alone. Knowing the terminology helps you negotiate better terms and spot deals designed for your situation.

Here are common leasing terms you'll encounter:

- Contract length: The lease duration, typically 6 to 24 months for flexible arrangements

- Early termination fee: Charges for ending your lease before the agreed date

- Fair wear and tear: Acceptable vehicle condition at return, excluding excessive damage

- Maintenance package: Optional coverage for servicing and repairs during the lease

- Soft credit check: A credit inquiry that doesn't affect your credit score

Pro Tip: Always ask leasing providers to explain any term you don't fully understand before signing. A reputable company welcomes questions and provides clear answers, whilst evasive responses signal potential problems. Write down unfamiliar terms during conversations and research them independently to verify explanations.

Understanding this foundation empowers you to evaluate offers critically and avoid agreements that don't suit your needs. The more confident you feel with the terminology, the better positioned you are to negotiate favourable terms and spot genuinely flexible deals.

How flexible lease terms help those with bad or limited credit

Flexible lease terms open doors for people traditional lenders reject. Contract length flexibility proves particularly valuable, with options ranging from 6 months to 24 months instead of the rigid 3 to 5 year agreements common in conventional leasing. Shorter contracts reduce long-term commitment, making approval easier for those with uncertain credit futures.

Flexible lease terms improve approval rates because they lower the leasing company's risk exposure. A 12-month agreement presents less risk than a 4-year commitment, encouraging providers to approve applicants they might otherwise decline. You also gain the freedom to upgrade or change vehicles more frequently as your business grows or personal circumstances evolve.

Early termination clauses provide escape routes if your situation changes unexpectedly. Whilst fees apply, knowing you can exit the agreement offers peace of mind. Some flexible providers structure these fees reasonably, charging only for remaining depreciation rather than punitive penalties. This flexibility proves invaluable for self-employed individuals whose income fluctuates or small businesses testing new markets.

No deposit leasing removes the biggest barrier for credit-challenged applicants: upfront costs. No deposit options improve financial accessibility by eliminating the need for thousands in savings. Instead of scraping together £2,000 to £5,000 upfront, you start driving immediately with just your first monthly payment.

Here's how to negotiate flexible lease terms effectively:

- Research multiple providers to compare flexibility offerings and identify the most accommodating terms

- Be honest about your credit situation upfront, as transparency builds trust and prevents wasted time

- Request shorter initial contracts with renewal options, demonstrating reliability before committing long-term

- Ask about soft credit checks that won't damage your score if you're declined

- Negotiate mileage allowances based on realistic usage, avoiding both excess charges and paying for unused miles

- Clarify early termination conditions and fees before signing, ensuring you understand exit costs

"Flexible leasing arrangements have increased approval rates for bad credit applicants by 40% compared to traditional fixed-term contracts, with shorter lease periods and no deposit requirements proving most effective."

Watch for providers offering genuine flexibility versus those using the term as marketing spin. True flexibility includes reasonable early termination terms, adjustable mileage allowances, and transparent fee structures. Companies genuinely supporting bad credit customers provide clear documentation and don't hide charges in fine print.

Pro Tip: Review the entire contract before signing, paying special attention to sections covering early termination, excess mileage, and damage charges. These areas often contain the costliest surprises. If anything seems unclear or unreasonable, negotiate changes or walk away. A good deal today shouldn't become a financial burden tomorrow.

Flexible terms transform van leasing from an exclusive product into an accessible solution for people rebuilding credit or managing variable incomes. The key lies in understanding which flexibility features matter most for your situation and finding providers who deliver them genuinely.

Common pitfalls in van leasing terminology and how to avoid them

Misunderstanding leasing terminology costs UK drivers thousands annually through unexpected charges and unsuitable agreements. The most common mistake involves underestimating mileage needs, leading to painful excess charges when you exceed your allowance. A van driver covering 15,000 miles yearly but signing for 10,000 miles faces £500 to £1,250 in penalties at 10p to 25p per excess mile.

Contract penalties catch many by surprise, particularly early termination fees and damage charges. Some agreements define "fair wear and tear" so narrowly that normal business use triggers charges. Others impose termination fees equalling 50% to 100% of remaining payments, effectively trapping you in unsuitable agreements.

Residual value confusion leads to poor decisions about contract length and monthly payments. Misunderstanding contract terms causes unexpected charges, particularly when residual values prove optimistic and you face additional fees at contract end. Some providers inflate residual values to advertise lower monthly payments, then charge "excess depreciation" fees when the vehicle's actual value falls short.

| Common Pitfall | Smart Alternative |

|---|---|

| Choosing lowest monthly payment without checking terms | Compare total contract costs including all fees and restrictions |

| Underestimating annual mileage to save money | Select realistic mileage allowance based on actual needs plus 10% buffer |

| Ignoring early termination clauses | Prioritise contracts with reasonable exit terms if circumstances change |

| Accepting vague damage definitions | Request written clarification of acceptable wear and tear standards |

| Signing without reading full contract | Review every clause, especially sections covering charges and penalties |

For credit-impaired clients, shorter leases offer significant advantages despite slightly higher monthly costs. Short-term leasing avoids long commitments that might become unaffordable if your circumstances change. A 12-month lease provides flexibility to reassess and potentially negotiate better terms once you've demonstrated reliability.

Ask these critical questions before signing any lease agreement:

- What exactly constitutes excess wear and tear, and can you provide photographic examples?

- How do you calculate early termination fees, and what's the maximum I could pay?

- Does the quoted monthly payment include all charges, or are there additional fees?

- What happens if I exceed my mileage allowance partway through the contract?

- Can I adjust my mileage allowance during the lease if my needs change?

- Do you conduct hard or soft credit checks, and will this affect my credit score?

Many providers bury unfavourable terms in dense legal language, hoping you won't read carefully. Take your time reviewing contracts, and don't let anyone pressure you into signing immediately. Legitimate companies allow time for consideration and welcome questions.

Pro Tip: Check the fine print regarding cancellations and excess mileage before signing anything. These sections contain the most expensive surprises. If the provider seems reluctant to explain these terms clearly, consider it a red flag. Photograph or save every page of your contract for future reference, as disputes often hinge on specific clause interpretations.

Avoiding these pitfalls requires diligence and a healthy scepticism towards deals that seem too good to be true. The lowest monthly payment often comes with the highest total cost once you factor in restrictions and penalties. Focus on finding fair, transparent agreements that match your actual needs rather than chasing advertised bargains.

Practical steps to apply your van leasing knowledge in 2026

Turning terminology knowledge into successful leasing requires systematic evaluation and clear communication with providers. Start by creating a personalised checklist that reflects your specific needs, credit situation, and usage patterns. This structured approach prevents emotional decisions and ensures you compare offers fairly.

Follow these steps to secure lease approval despite bad credit:

- Calculate your realistic budget including monthly payments, insurance, fuel, and potential excess charges to avoid overcommitting

- Estimate annual mileage accurately by reviewing past vehicle usage or calculating business route requirements plus 10% buffer

- Research flexible leasing providers specialising in bad credit approvals rather than approaching mainstream companies likely to decline

- Gather documentation proving income stability, such as bank statements, tax returns, or employment contracts, even if not formally required

- Request soft credit checks first to avoid damaging your score with multiple hard inquiries across different providers

- Compare at least three detailed quotes including all fees, restrictions, and contract terms rather than focusing solely on monthly payments

- Negotiate terms openly, explaining your credit situation honestly and demonstrating how you'll meet obligations reliably

- Read the entire contract thoroughly, highlighting any unclear sections and requesting written clarification before signing

- Keep copies of all documentation, correspondence, and contract terms for future reference and dispute resolution

- Set up automatic payments to avoid missed payments that could further damage your credit and trigger default charges

Monitoring and adjusting lease usage prevents penalties and builds positive relationships with providers. Track your mileage monthly using a simple spreadsheet or smartphone app, ensuring you stay within allowances. If you approach your limit early, contact your provider immediately to discuss adjustment options. Most companies allow mileage increases mid-contract for an additional monthly fee, which costs less than excess charges.

Managing cash flow becomes easier when you understand exactly what you're paying for and when charges apply. Budget for your monthly payment plus a small contingency for potential excess mileage or minor damage charges. This conservative approach prevents financial stress and ensures you can meet obligations even during difficult months.

Documentation and communication prove essential throughout your lease. Photograph your van's condition at collection, noting any existing damage to avoid disputes at return. Keep service records meticulously, as some contracts require proof of proper maintenance. When issues arise, communicate with your provider promptly in writing, creating a paper trail that protects both parties.

Maintain regular contact with your leasing provider, especially if you anticipate difficulties meeting payments. Most companies prefer working with customers proactively rather than pursuing defaults. If your circumstances improve, ask about opportunities to upgrade or extend your lease, building a positive relationship that benefits future applications.

Document every interaction with your provider, including phone calls, noting the date, time, person you spoke with, and what was discussed. This record proves invaluable if disputes arise about agreed terms or verbal promises. Email confirmations work even better, providing written evidence of agreements.

Applying your terminology knowledge transforms you from a passive consumer into an informed negotiator. You'll spot unfavourable terms immediately, ask questions that reveal hidden costs, and select agreements genuinely suited to your needs. This confidence helps you navigate the leasing process successfully despite credit challenges, securing flexible arrangements that support your goals rather than creating additional financial stress.

Find flexible van leasing options with Flexi Auto Lease

Now that you understand van leasing terminology, finding the right provider becomes straightforward. Flexi Auto Lease specialises in flexible leasing solutions for UK individuals and small businesses facing credit challenges. We focus on what matters: your ability to afford monthly payments, not just your credit history.

Our process removes traditional barriers through soft credit checks that don't affect your score, no deposit options that eliminate upfront costs, and flexible contract lengths from 6 to 24 months. We deliver nationwide, include road tax and maintenance in transparent pricing, and approve applications quickly so you can drive within days.

Key benefits include:

- Flexible terms designed specifically for bad and limited credit applicants

- No deposit options that protect your cash flow

- Quick approval processes with decisions often within 24 hours

- All-inclusive pricing covering road tax, maintenance, and breakdown cover

- Dedicated support team answering questions throughout your lease

Visit Flexi Auto Lease today to explore current van deals and receive a personalised quotation based on your specific needs. Our straightforward three-step process lets you browse vehicles, apply online, and start driving quickly. Whether you need a van for personal use or your growing business, we'll find a flexible solution that works for your situation.

FAQ

What is the difference between leasing and hiring a van?

Leasing typically involves longer-term contracts with fixed monthly payments and lower daily costs, whilst hiring offers short-term access at higher rates. Leasing suits ongoing business use where you need consistent vehicle access, whereas hiring works for temporary projects or occasional needs. Understanding these differences helps you choose the most cost-effective option for your situation.

Can I get approved for van leasing with bad credit in the UK?

Approval chances increase significantly with flexible leasing terms and no deposit options designed for credit-challenged applicants. Specialist providers focus on affordability and income stability rather than credit scores alone, making approval possible even with previous financial difficulties. Flexible options specifically support bad credit applicants through soft credit checks and shorter contract periods that reduce provider risk.

What does no deposit leasing mean?

No deposit leasing means starting your lease without any upfront payment beyond your first monthly instalment, eliminating the typical £2,000 to £5,000 deposit requirement. This approach improves accessibility for applicants with limited savings or credit history by spreading all costs across monthly payments. You can start driving immediately without depleting cash reserves needed for business operations or emergencies.

How important is the mileage allowance in a van lease?

Mileage allowance critically affects your total lease cost because exceeding it triggers penalty charges of 10p to 25p per excess mile. Selecting the right allowance from the start prevents expensive surprises, so calculate your realistic annual mileage and add a 10% buffer for unexpected journeys. Underestimating to save on monthly payments often costs more overall once excess charges apply at contract end.