Many believe securing a van with poor credit means accepting rejection or sky-high deposits. That's not true anymore. Flexible short-term van leasing has transformed access for UK individuals with bad or limited credit histories, offering accessible alternatives to traditional van hiring with higher approval rates, predictable costs, and minimal credit score impact.

Table of Contents

- Introduction To Van Leasing And Hiring

- Credit And Eligibility Considerations For Bad Credit Customers

- Cost And Contract Flexibility Comparison

- Common Misconceptions About Van Leasing And Hiring

- Practical Benefits And Use Cases For Bad Credit Customers

- How To Choose Between Van Leasing And Hiring

- Discover Flexible Van Leasing Solutions For Bad Credit

- FAQ

Key Takeaways

| Point | Details |

|---|---|

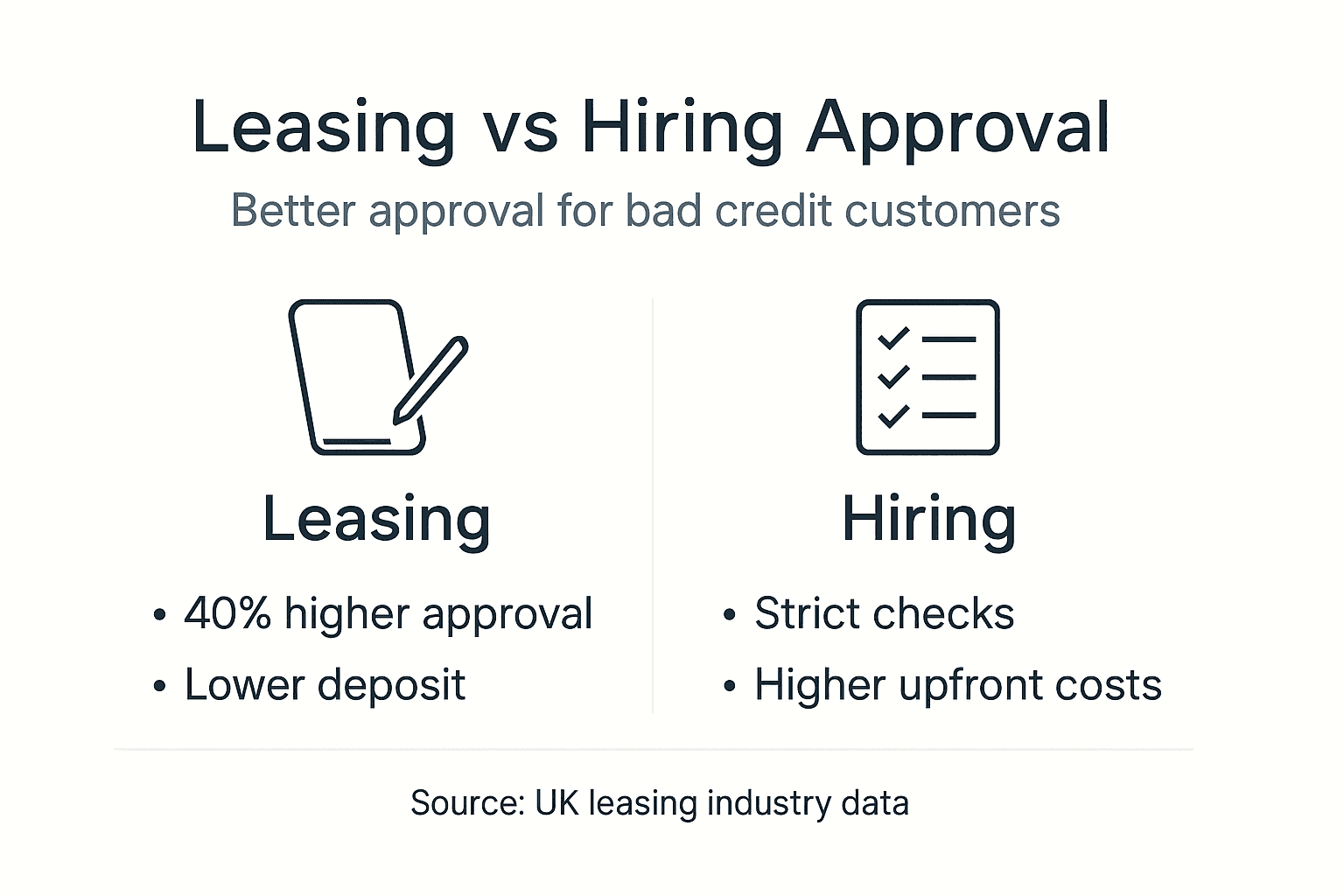

| Leasing approval rates | Flexible leasing providers reject fewer than 15% of bad credit applicants compared to 60% refusal rates in traditional hiring. |

| Credit check differences | Leasing commonly uses soft credit checks that don't harm your score, while hiring typically requires hard checks. |

| Cost structure | Leasing offers fixed monthly payments including road tax, maintenance, and insurance, eliminating surprise expenses. |

| Contract flexibility | Leasing suits 6 to 24 month needs; hiring works best for under one week unpredictable use. |

| Financial predictability | Leasing provides better cash flow management with bundled services, while hiring charges higher daily rates. |

Introduction to Van Leasing and Hiring

Understanding the fundamental differences between van leasing and hiring helps you make informed choices suited to your credit situation and transport needs. Van leasing is a contract-based arrangement where you pay fixed monthly fees to use a vehicle for a set period, typically between 6 and 24 months. The leasing company retains ownership while you enjoy full use of the van throughout the term.

Van hiring operates differently. It's a flexible short-term rental without long-term contractual commitments, allowing you to rent a van for anything from a single day to several weeks. You pay daily or weekly rates, return the vehicle when finished, and walk away with no ongoing obligations.

Contract lengths vary significantly between these options:

- Leasing contracts run from 6 months minimum up to 24 months

- Hiring allows day-to-day or week-to-week flexibility with no fixed term

- Some flexible leasing providers now offer shorter 3 month terms for specific needs

Leasing suits predictable, ongoing transport requirements like regular business deliveries, project work spanning several months, or extended personal use. Hiring works better for one-off jobs, weekend moves, or covering temporary vehicle breakdowns.

The UK market offers numerous flexible short-term leasing providers specifically targeting customers with poor credit histories. These companies recognize that traditional credit scoring doesn't reflect everyone's ability to make regular payments. They've built approval processes around affordability and income verification rather than just credit scores.

For bad credit customers, this distinction matters enormously. Traditional van hire companies often apply strict credit checks that result in automatic rejections or demand prohibitive deposits. Flexible leasing providers take a different approach, making van access realistic even with past credit challenges.

Credit and Eligibility Considerations for Bad Credit Customers

Credit requirements represent the most significant difference between van leasing and hiring for individuals with poor credit histories. Credit considerations in van rental vs leasing show many individuals with poor or limited credit histories face high deposits or outright rejection when hiring vans traditionally, but leasing options with flexible credit policies lower barriers substantially.

Leasing companies focused on bad credit customers commonly use soft credit checks. These checks review your credit file without leaving a visible footprint that impacts your credit score. Hard credit checks, used by most traditional hire companies, create a recorded search on your credit report that temporarily lowers your score and signals risk to other lenders.

The approval rate differences are stark:

- Traditional van hire companies reject approximately 60% of bad credit applicants or require deposits exceeding £1,000

- Flexible leasing providers specializing in poor credit reject fewer than 15% of applicants

- Deposit requirements for bad credit leasing typically range from £200 to £500

- Some leasing companies approve applicants with CCJs, IVAs, or bankruptcies discharged over 12 months ago

Deposit structures also differ fundamentally. Hire companies view deposits as risk mitigation for potential vehicle damage or non-payment, setting amounts based on credit risk assessment. High-risk customers face higher deposits. Leasing deposits function more like initial payments, with amounts determined by vehicle value and contract length rather than solely credit score.

Pro tip: Seek leasing providers advertising bad credit friendly terms and soft checks to improve approval chances. Check whether they offer decisions in principle without affecting your credit score, allowing you to explore options safely before committing.

Income verification matters more than credit scores for flexible leasing. Providers want evidence you can afford monthly payments through bank statements, payslips, or accounts for self-employed applicants. Demonstrating stable income, even with poor credit history, often secures approval where traditional hire companies would refuse.

Cost and Contract Flexibility Comparison

Financial structures differ dramatically between leasing and hiring, affecting both upfront costs and long-term value. Understanding these differences helps you calculate true costs and avoid expensive surprises.

Leasing offers fixed monthly payments that bundle multiple costs into one predictable fee. Your monthly payment typically includes:

- Road tax for the entire contract period

- Comprehensive maintenance and servicing

- Breakdown cover and recovery services

- Full insurance in some packages

- Delivery to your UK address

Hiring charges daily rates that appear cheaper initially but exclude critical costs. Most hire agreements require you to arrange and pay separately for insurance, fuel, and any damage repairs. Hidden fees often include mileage charges beyond daily limits, cleaning fees, late return penalties, and admin charges.

Van hire vs leasing cost comparison data reveals van hire daily rates can be up to 25% higher than short-term van leasing monthly equivalents when you account for all included services.

Here's a practical cost comparison:

| Duration | Leasing Monthly Cost | Hiring Total Cost | Leasing Advantage |

|---|---|---|---|

| 1 week | N/A (minimum 6 months) | £350 to £500 | Not applicable |

| 1 month | £300 to £450 (all-inclusive) | £900 to £1,400 (basic rate plus insurance) | 40% to 50% savings |

| 6 months | £1,800 to £2,700 total | £5,400 to £8,400 total | 65% to 70% savings |

| 12 months | £3,600 to £5,400 total | £10,800 to £16,800 total | 65% to 70% savings |

Contract flexibility represents the key trade-off. Hiring allows you to rent for exactly the period needed, from one day upward, with no long-term commitment. You can hire different van sizes for different jobs. Leasing requires minimum 6 month commitments in most cases, though some flexible providers offer 3 month terms.

Pro tip: Calculate total expected costs including hidden fees before deciding. Request itemized quotes showing all charges, mileage limits, insurance requirements, and early termination penalties. For needs exceeding one month, leasing almost always costs less overall.

Cash flow predictability makes leasing attractive for businesses and individuals on tight budgets. Fixed monthly payments simplify budgeting without surprise bills for repairs or maintenance. Hiring creates unpredictable costs when vehicles need service or encounter problems during your rental period.

Early termination provisions differ too. Leasing contracts typically require you to pay remaining months or substantial early exit fees. Hiring lets you return the van anytime, though you lose any upfront booking discounts or weekly rate benefits.

Common Misconceptions About Van Leasing and Hiring

Several persistent myths about van leasing and hiring confuse customers with bad credit, leading them toward unsuitable or expensive choices. Let's correct these misunderstandings.

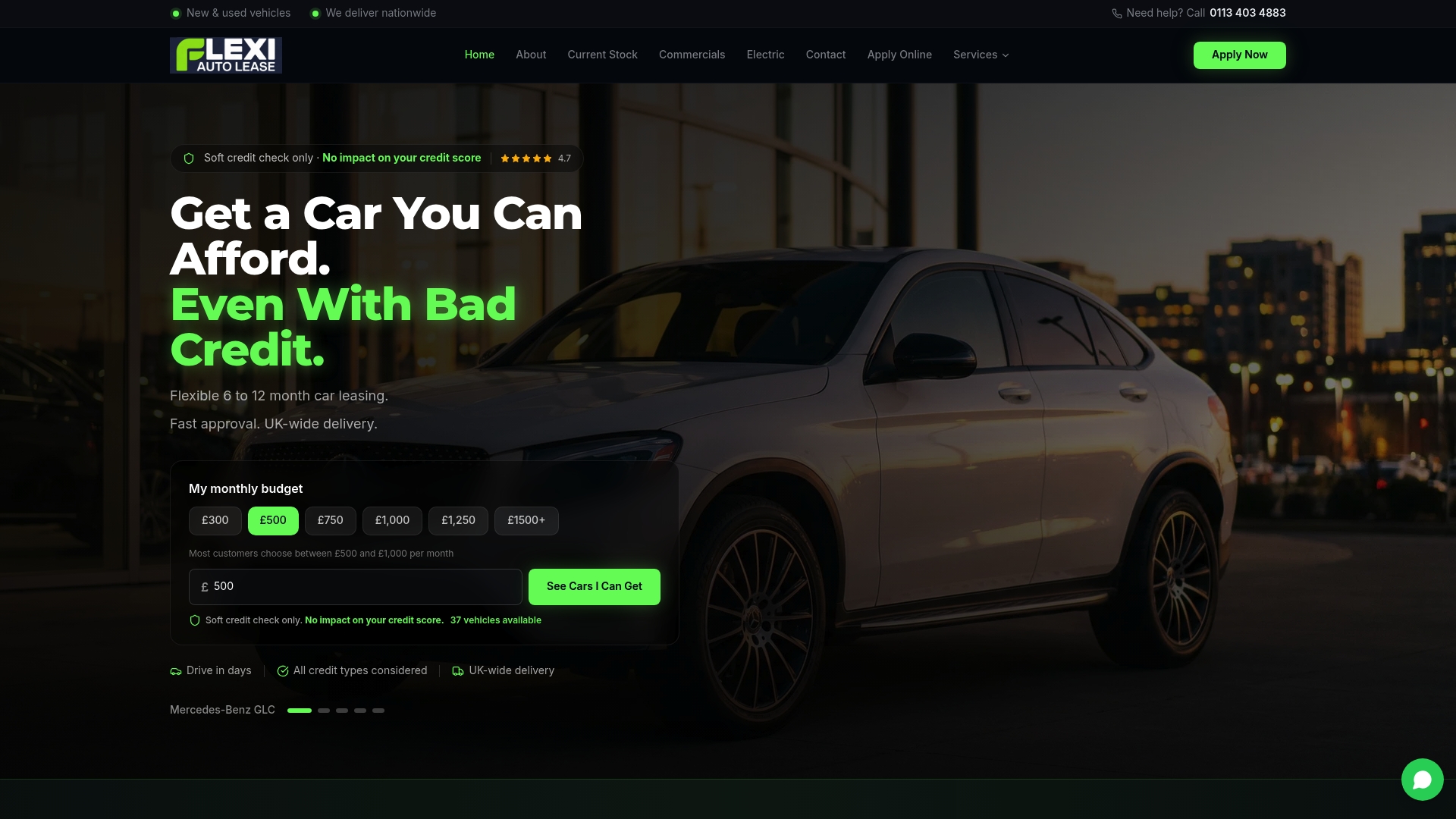

Misconception one: Leasing always requires excellent credit scores. Many flexible leasing providers specifically serve bad credit customers using soft credit checks and affordability-based approvals. Your credit history matters less than your current income and ability to make regular payments. Companies like Flexi Auto Lease exist precisely to serve customers traditional lenders reject.

Misconception two: Hiring is always cheaper and more flexible. While hiring offers day-to-day flexibility, it costs significantly more for periods beyond one week. The apparent flexibility disappears when you need a van for several months and face mounting daily charges. Leasing provides better value and predictability for extended use.

Misconception three: Leasing involves hidden fees and surprise costs. Quality leasing providers bundle everything into transparent monthly payments covering tax, maintenance, and breakdown cover. You know your exact cost upfront with no surprises. Hiring actually involves more hidden fees through mileage charges, cleaning costs, and insurance excess payments.

Misconception four: Soft credit checks don't work properly, so lenders charge more. Soft checks provide sufficient information for approval decisions without damaging your credit score. Flexible leasing providers use additional verification like bank statements and income proof. Rates reflect vehicle costs and contract length, not credit check type.

Misconception five: You can't lease if you have CCJs, IVAs, or past bankruptcies. Many flexible providers approve customers with these credit issues if they've been discharged for 12 months or more and you demonstrate current affordability. Each application receives individual assessment rather than automatic computer rejection.

Key points to remember:

- Bad credit leasing options genuinely exist with reasonable approval rates

- Hiring flexibility comes with significant cost penalties for longer use

- Leasing bundles more services, reducing unexpected expenses

- Credit score impact differs substantially between soft and hard checks

Understanding these realities helps you avoid costly mistakes and find solutions actually suited to your credit situation and transport needs.

Practical Benefits and Use Cases for Bad Credit Customers

Flexible van leasing delivers tangible advantages for UK individuals and businesses struggling with poor credit histories. These benefits extend beyond just vehicle access to include financial stability and business growth opportunities.

Predictable monthly payments reduce financial stress significantly. When you know exactly what you'll pay each month with no surprise repair bills or insurance excess charges, budgeting becomes straightforward. This certainty helps you manage other financial commitments without worrying about unexpected van costs derailing your budget.

Flexible leasing benefits for bad credit customers research confirms flexible leasing offers faster approval and nationwide access regardless of location, aiding bad credit customers.

Faster approval processes mean you can access needed transport within days rather than weeks. Traditional vehicle finance requires extensive credit checks and documentation that delay decisions. Flexible leasing providers make approval decisions in hours, with vehicles delivered nationwide within 48 to 72 hours of acceptance.

Real-world use cases demonstrate leasing's value:

- Small business owners launching delivery services without capital for van purchases

- Self-employed tradespeople needing reliable transport after credit setbacks

- Individuals requiring temporary van access for house moves or project work spanning several months

- Businesses testing new service offerings before committing to vehicle purchases

- Companies expanding into new regions needing vehicles quickly without long approval waits

Geographic flexibility helps customers across all UK regions. Whether you live in rural Scotland, urban London, or anywhere between, leasing providers deliver vehicles to your location. This nationwide reach removes the barrier of needing to travel for vehicle collection, especially important when public transport access limits your options.

Customers with bad credit consistently report leasing improved their access to necessary vehicles with lower deposits and minimal credit score impact. The soft check approach means exploring leasing options doesn't harm your ability to secure other credit later. Each successful monthly payment can actually help rebuild your credit profile over time.

Business growth becomes possible when poor credit doesn't block access to essential commercial vehicles. Flexible leasing lets you scale operations, take on larger contracts, and serve more customers without the catch-22 of needing good credit to grow the business that improves your credit.

How to Choose Between Van Leasing and Hiring

Applying a structured decision framework ensures you select the option truly suited to your circumstances, credit status, and transport requirements. Follow these steps:

-

Assess your credit situation honestly. Check your credit report to understand your score and any adverse markers like CCJs or defaults. If your score falls below 600 or you have recent adverse credit, flexible leasing represents your best approval path. Above 700 with clean history, traditional hiring may approve you, but leasing still often costs less.

-

Determine intended van usage duration and frequency. Calculate how long you need the vehicle. Under one week suggests hiring. One to three months creates a grey area where flexible short-term leasing might work. Over three months clearly favors leasing for cost savings and convenience. Consider whether your need is one-off or recurring.

-

Compare total all-in costs including tax, insurance, and maintenance. Request itemized quotes from both leasing and hiring providers. Add up every cost over your intended usage period including insurance, fuel, mileage charges, and potential damage excess. Don't just compare daily hire rates to monthly lease payments without accounting for bundled services.

-

Examine credit check types and deposit needs of providers. Ask explicitly whether companies use soft or hard credit checks. Confirm deposit amounts and whether they're refundable. Calculate your total upfront cost including first payment and deposit. Bad credit typically means choosing providers using soft checks to protect your credit score.

-

Balance credit impact, cost predictability, and flexibility priorities. Decide what matters most for your situation. If protecting your credit score is paramount, choose soft-check leasing. If day-to-day flexibility outweighs cost, consider hiring despite higher expense. If budget predictability is critical, leasing's fixed payments suit you best.

-

Apply decision rules based on your analysis. Hire for under one week when you need maximum flexibility and have good credit for approval. Lease for one to 24 months when you have poor credit, need cost certainty, or want bundled services. For one to four weeks with good credit, hiring might work if you calculate total costs carefully.

-

Test your decision against worst-case scenarios. What if the van needs repairs during hire? Can you afford the excess? What if your leasing circumstances change and you need to exit early? Can you manage termination fees? Stress-testing your choice reveals potential problems before commitment.

This structured approach transforms a confusing choice into a logical decision aligned with your financial reality and practical needs. Take time to work through each step thoroughly rather than rushing into whichever option seems superficially cheaper or easier.

Discover Flexible Van Leasing Solutions for Bad Credit

You now understand how van leasing and hiring differ for bad credit customers. Flexible leasing removes traditional barriers, offering accessible transport regardless of your credit history.

Explore short-term van leasing options with soft credit checks and all-inclusive pricing. Access vehicles across the UK within days, benefit from predictable monthly payments covering tax and maintenance, and protect your credit score with approval processes designed for bad credit customers. Whether you need commercial vans for business growth or temporary transport solutions, flexible leasing terms from 6 to 24 months provide the accessibility and affordability you need without the credit barriers that block traditional options.

FAQ

What credit checks are used in van leasing and hiring?

Leasing providers focused on bad credit customers mainly use soft credit checks that don't impact your credit score. These checks review your credit file without leaving visible footprints. Traditional van hire companies typically use hard credit checks that temporarily lower your score and appear on your credit report.

Can I lease a van if I have bad credit?

Yes, many UK leasing providers specialize in bad credit approvals with flexible terms and lower deposits. Companies like Flexi Auto Lease use soft credit checks and affordability assessments rather than relying solely on credit scores, approving over 85% of applicants regardless of credit history.

Is van hiring more cost-effective than leasing?

Hiring costs less only for very short-term use under one week. For periods of one month or longer, leasing saves 40% to 70% compared to cumulative hire charges because monthly payments bundle tax, maintenance, and insurance that hiring excludes. Calculate total all-in costs over your intended period to compare accurately.

What contract lengths are typical for van leasing?

Leasing contracts usually run from 6 to 24 months, with some flexible providers offering 3 month minimum terms. Hiring offers maximum flexibility with no long-term commitment, allowing daily or weekly rentals. Shorter flexible leases increasingly available specifically serve bad credit clients needing accessible medium-term transport solutions.