Many believe bad credit makes van leasing impossible, especially without a deposit. This misconception stops countless UK small business owners and self-employed individuals from exploring flexible leasing solutions that could transform their operations. The reality is far more encouraging. Flexible van leasing options exist in 2026 specifically designed for those with bad or limited credit histories, often with minimal or no deposit requirements. You will discover how these arrangements work, what costs to expect, how to protect your credit score, and practical strategies to secure the right van lease for your circumstances.

Table of Contents

- Understanding Bad Credit Van Leasing Options In The UK

- Low And No Deposit Van Leasing Explained: Benefits And Costs

- Common Misconceptions And Hidden Costs In Bad Credit Van Leasing

- Tips For Securing Flexible Van Leasing With Bad Credit In 2026

- Find Flexible Van Leasing Solutions With Flexi Auto Lease

Key takeaways

| Point | Details |

|---|---|

| Cash flow preservation | Low or no deposit van leasing reduces upfront financial burden, helping small businesses allocate funds to other essential operational needs. |

| Higher monthly costs | Expect increased monthly payments when choosing no deposit options, as lenders offset the reduced upfront risk over the lease term. |

| Hidden fees exist | Administration charges, wear and tear costs, and excess mileage penalties can significantly increase total leasing expenses beyond advertised rates. |

| Approval is possible | Flexible lenders specialise in bad credit van leasing, though stricter criteria and documentation requirements typically apply. |

| Credit protection matters | Limiting credit enquiries and choosing soft check lenders helps protect your credit score during the application process. |

Understanding bad credit van leasing options in the UK

Bad credit typically refers to credit scores below 580 on most UK scoring systems, often resulting from missed payments, defaults, County Court Judgements, or limited credit history. When you apply for van leasing with bad credit, lenders scrutinise your financial background more intensively than they would for applicants with strong credit profiles. This heightened scrutiny becomes especially pronounced for no deposit arrangements, where lenders face greater risk by providing vehicles without substantial upfront security.

Good credit scores facilitate approval for no deposit van leasing, while poor credit can complicate or block the process entirely. However, this does not mean leasing remains out of reach. Specialist lenders in the UK market have developed flexible products specifically for individuals and businesses with credit challenges. These providers recognise that credit history does not always reflect current financial stability or future payment capability.

When approaching van leasing with bad credit, set realistic expectations. You will likely face:

- Higher monthly payments compared to standard leases

- Requirements for some initial payment, even in 'no deposit' deals

- More extensive documentation requests to verify income and business viability

- Shorter lease terms to reduce lender risk exposure

- Potentially limited vehicle choice compared to prime credit customers

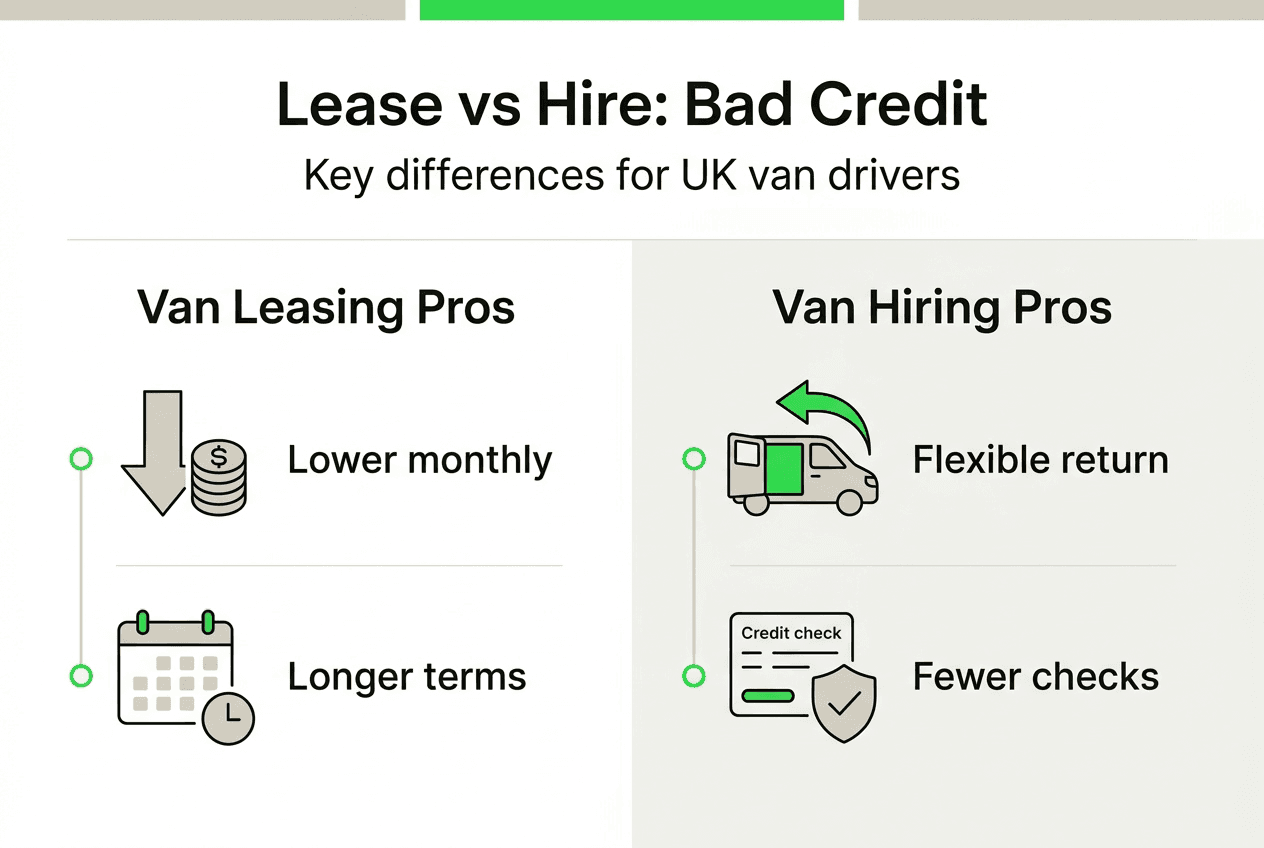

The distinction between van leasing and hiring for bad credit becomes important here. Leasing typically offers better approval rates for those with credit challenges because the arrangement spreads risk over longer periods with contractual commitments. Hiring, whilst more flexible, often requires stronger credit profiles for short term arrangements. Understanding these nuances helps you target the right financing approach for your situation.

Low and no deposit van leasing explained: benefits and costs

Low or no deposit van finance helps preserve crucial cash flow, allowing businesses to allocate funds to other essential needs such as inventory, marketing, or operational expenses. For small businesses and self-employed individuals operating on tight margins, this cash flow preservation can mean the difference between seizing growth opportunities and struggling with liquidity constraints.

The financial trade off, however, is significant. Monthly payments for no deposit arrangements are typically higher than standard leases, sometimes by 15 to 25 percent. Lenders compensate for the increased risk and reduced upfront security by spreading these costs across your monthly obligations. Over a 24 month lease, this difference can add hundreds or even thousands of pounds to your total cost.

Beyond monthly payments, watch for these additional costs:

- Administration and processing fees, often £100 to £300

- Wear and tear charges assessed at lease end

- Excess mileage penalties if you exceed agreed annual limits

- Maintenance responsibilities unless explicitly included in your agreement

- Early termination fees if circumstances change

Pro Tip: Request a complete cost breakdown showing all fees, charges, and potential penalties before signing any lease agreement. This transparency helps you compare offers accurately and avoid budget surprises.

The table below illustrates typical monthly payment differences across deposit levels for a standard small van lease:

| Deposit amount | Monthly payment | Total cost (24 months) |

|---|---|---|

| £0 (no deposit) | £385 | £9,240 |

| £500 (low deposit) | £350 | £8,900 |

| £1,500 (standard) | £295 | £8,580 |

These figures demonstrate how no deposit leasing benefits your immediate cash position whilst increasing overall expenditure. The decision ultimately depends on your current financial priorities and whether preserving working capital justifies the premium.

Common misconceptions and hidden costs in bad credit van leasing

The term 'no deposit' can be misleading, as initial payments are often required despite the marketing language. These initial costs typically include the first month's rental payment, which can range from £250 to £500 or more depending on the vehicle and lease terms. Some agreements also require an administration fee upfront, blurring the line between 'no deposit' and traditional leasing structures.

This semantic confusion creates unrealistic expectations. When you see 'no deposit' advertised, understand it usually means no large lump sum equivalent to several months' payments, not zero upfront cost. Always clarify exactly what you will pay before driving away, including any processing charges, documentation fees, or advance rental requirements.

Several fees beyond initial payments can apply, including:

- Wear and tear assessments based on British Vehicle Rental and Leasing Association guidelines

- Maintenance costs if not included in your package

- Excess mileage penalties, often 5p to 15p per mile over agreed limits

- Broker fees if using intermediaries to arrange your lease

- Application fees charged by some lenders regardless of approval outcome

- Early termination charges if you need to exit the lease prematurely

Brokers and intermediaries add another layer of potential costs. Whilst they can help navigate the bad credit leasing landscape, their services come at a price, sometimes hidden within inflated monthly payments or charged as separate arrangement fees. Not all brokers disclose their commission structures transparently, making true cost comparison difficult.

Pro Tip: Before signing any lease agreement, request a comprehensive written breakdown of every charge you will face over the lease term, including potential penalties. Ask specifically about wear and tear assessment criteria, mileage limits, and early termination costs. Understanding van leasing terminology helps you ask the right questions and interpret contract language accurately.

Read contract terms with particular attention to maintenance responsibilities, insurance requirements, and end of lease obligations. These clauses often contain costly surprises for those who skim the fine print. If terminology seems unclear, request plain English explanations before committing.

Tips for securing flexible van leasing with bad credit in 2026

Lenders may have stricter criteria for no deposit van finance due to the higher risk involved, scrutinising credit scores and business financial history more intensively than standard applications. Understanding these requirements and preparing accordingly significantly improves your approval chances.

Follow these steps to maximise your leasing success:

- Check your credit report from all three UK credit reference agencies (Experian, Equifax, TransUnion) to identify and dispute any errors that might unfairly damage your score.

- Calculate a realistic monthly budget that accounts for higher payments typical of bad credit leases, ensuring you can comfortably meet obligations without financial strain.

- Consider short term leasing options of 6 to 12 months, which often have more flexible approval criteria and allow you to build positive payment history.

- Gather comprehensive financial documentation including bank statements, tax returns, and proof of income to demonstrate current financial stability despite past credit challenges.

- Research your vehicle needs carefully to avoid applying for more expensive vans than necessary, as lower value leases typically face easier approval.

Additional strategies include:

- Seeking brokers or lenders specialising in bad credit van finance who understand your circumstances and have established relationships with flexible funders

- Preparing detailed business plans or income projections if self-employed to demonstrate future payment capability

- Considering guarantors with stronger credit profiles to support your application and potentially secure better terms

- Comparing multiple quotes from different providers to identify the most competitive rates and favourable terms

- Asking specifically about soft credit check options that assess eligibility without impacting your credit score

Minimising credit enquiries protects your score during the search process. Each hard credit check can temporarily reduce your score by a few points, and multiple applications within a short period raise red flags for lenders. Concentrate your applications within a focused timeframe, ideally securing pre-approval or soft check assessments before formal applications.

Pro Tip: Apply these small business leasing tips even if you operate as a sole trader. Presenting your van needs as business transportation rather than personal use can open additional financing options and potentially improve terms. Prepare a simple business case explaining how the van supports your income generation.

When comparing quotes, look beyond monthly payment figures. Examine total cost over the lease term, included services like maintenance and road tax, mileage allowances, and flexibility for early termination or lease extension. The cheapest monthly payment rarely represents the best overall value, especially when hidden fees and restrictions apply.

Find flexible van leasing solutions with Flexi Auto Lease

Navigating bad credit van leasing requires expertise, patience, and access to lenders who understand your situation. Flexi Auto Lease specialises in providing flexible van leasing solutions for individuals and small businesses with bad or limited credit across the UK. Our approach focuses on your current financial stability and future payment capability rather than dwelling exclusively on past credit challenges.

We offer tailored leasing options including low and no deposit plans designed to preserve your working capital whilst getting you on the road quickly. Our soft credit check process protects your credit score during initial assessment, and our nationwide delivery service brings your chosen van directly to your location. With all-inclusive pricing covering road tax and maintenance, you gain predictable monthly costs without unexpected expenses. Explore personalised quotes matching your specific financial needs and vehicle requirements, or contact our specialist team for expert guidance through every step of the leasing process.

FAQ

Can I lease a van with bad credit in the UK?

Yes, flexible leasing options exist for bad credit in the UK, though you should expect higher monthly payments and potentially some initial fees. Specialist lenders focus on current affordability rather than past credit issues. Approval depends on demonstrating stable income and meeting the lender's specific criteria, which vary between providers.

What does no deposit van leasing really mean?

No deposit typically means no large upfront lump sum equivalent to multiple months' payments, but initial fees like first month's rental usually apply. Read contract terms carefully to understand exactly what you pay before taking delivery. True zero cost arrangements are extremely rare, especially for bad credit applicants.

How can I protect my credit score when leasing a van?

Limit credit enquiries by researching thoroughly before applying and using soft check services where available. Choose flexible leases with minimal commitments and prepare comprehensive financial documentation to speed approval and reduce the need for multiple applications. Concentrate applications within a short timeframe to minimise score impact.

Are monthly payments much higher with bad credit van leasing?

Yes, expect monthly payments 15 to 25 percent higher compared to standard leases with good credit. This premium compensates lenders for increased risk and reduced upfront security. The exact increase depends on your specific credit situation, chosen vehicle, lease term, and deposit amount.

What hidden costs should I watch for in van leasing agreements?

Administration fees, wear and tear charges, excess mileage penalties, and broker commissions frequently add significant costs beyond advertised rates. Early termination fees and maintenance responsibilities can also create unexpected expenses. Always request a complete written breakdown of all potential charges before signing any agreement.