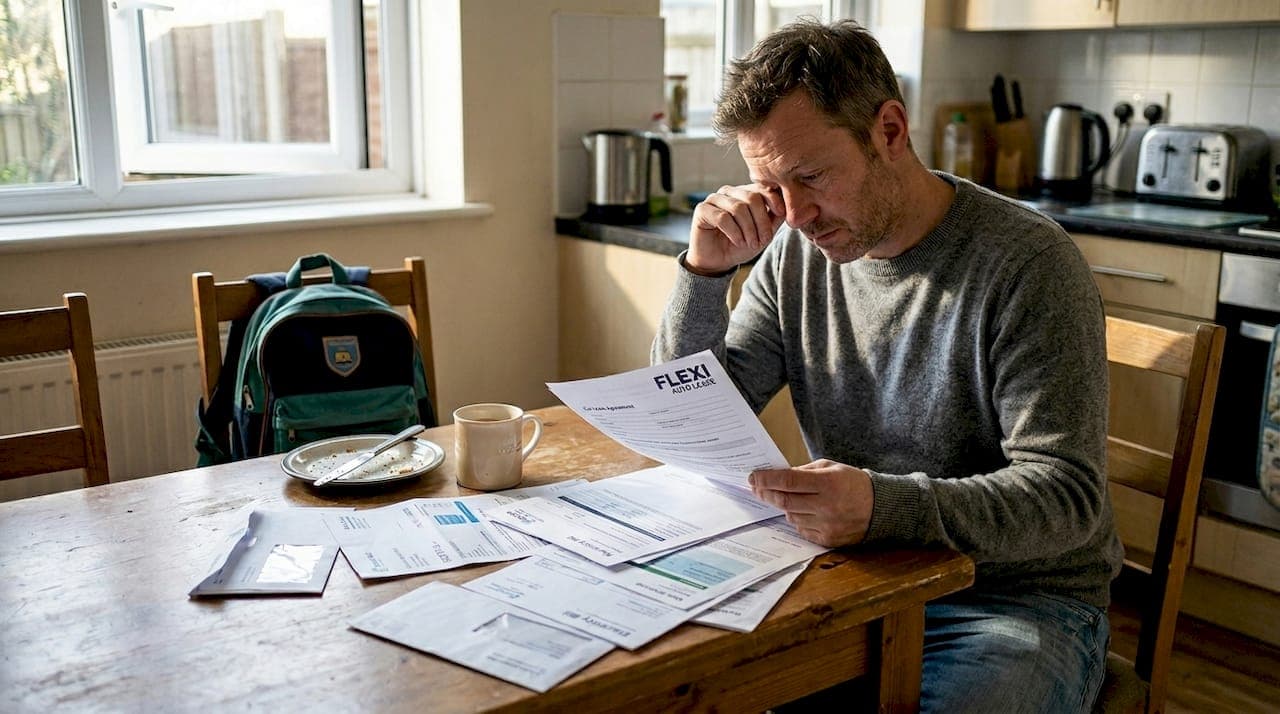

Getting behind the wheel when your credit history isn't perfect can feel like hitting a wall. Whether you're a sole trader needing a van or an individual looking for a reliable car, complex leasing terms and credit barriers can seriously limit your options. The good news is that negotiating flexible vehicle leasing terms of 6 to 24 months is genuinely possible, even with bad or limited credit. This guide walks you through every stage, from understanding your options to signing a fair contract, without damaging your credit score in the process.

Table of Contents

- Understand your leasing options with bad credit

- Prepare your negotiation toolkit: requirements and documents

- Step-by-step guide to negotiating car lease terms

- Common pitfalls and how to avoid them

- What success looks like: outcomes and next steps

- Our take: why flexibility in negotiation beats chasing the lowest price

- Ready to negotiate your next flexible lease?

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Know your options | Bad or limited credit doesn’t mean you can’t lease—a range of short-term solutions is available in the UK. |

| Preparation matters | Gathering the right documents and upfront payment options increases your negotiating power. |

| Negotiation steps | Be transparent, negotiate upfront terms, and use practical tactics for the best agreement. |

| Watch for pitfalls | Check for hidden costs, inflexible terms, and tax issues before signing your lease. |

| Prioritise flexibility | Choosing flexible terms helps you adapt to changes and avoid costly mistakes. |

Understand your leasing options with bad credit

With your need for flexibility clear, let's examine what leasing options you have if your credit isn't perfect.

There are several routes available to you, and knowing the difference between them is essential before you approach any provider. The main options are personal contract hire (PCH), business contract hire (BCH), standard fixed-term leases, and short-term leases running from 6 to 24 months. Each has its own approval criteria, credit check process, and exit conditions.

For most people with bad or limited credit, bad credit leasing options that sit in the short-term category offer the best balance of risk and flexibility. Shorter contracts mean lower total exposure for the lender, which can make approval more achievable. They also protect you if your circumstances change.

According to leasing with bad credit guidance, higher upfront payments of 1 to 12 months, choosing a cheaper car, using a guarantor, or exploring lease takeovers are all practical strategies. Expect higher monthly rates and stricter terms, but approval is achievable.

Here's a quick comparison of the main lease types:

| Lease type | Best for | Credit check | Flexibility |

|---|---|---|---|

| PCH | Individuals | Hard check | Low to medium |

| BCH | Businesses | Business credit check | Medium |

| Short-term lease | Both | Soft or no check | High |

| Lease takeover | Both | Varies | Medium |

The benefits of short-term leases are particularly strong for those managing uncertain finances:

- Lower commitment period reduces financial risk

- Easier to exit or renew without heavy penalties

- Providers are often more willing to approve shorter terms

- Ideal for seasonal business needs or probationary employment periods

A guarantor, typically someone with a stronger credit profile, can also significantly improve your approval odds on longer contracts if you need them.

Prepare your negotiation toolkit: requirements and documents

Knowing your options is just the start; proper preparation sets the stage for successful negotiation.

Walking into a lease negotiation without the right paperwork is one of the most common mistakes people make. Providers need confidence that you can meet your payments, and your documents are how you build that confidence.

For individuals, you'll typically need:

- Proof of identity (passport or driving licence)

- Proof of address (utility bill or bank statement, dated within 3 months)

- Three to six months of bank statements

- Proof of income (payslips or benefits letters)

- Details of any existing credit commitments

For small businesses and sole traders, business car leasing requirements go further. If you're VAT-registered with one to two years of trading history, you may qualify for BCH, which is tax deductible and VAT reclaimable at 50 to 100% depending on business use. You'll also need your business registration details, recent accounts or self-assessment returns, and VAT registration number if applicable.

Presenting this information clearly and proactively signals to the provider that you're organised and serious. It also reduces back-and-forth delays that can slow approval.

Here's a quick reference table for document requirements:

| Document | Individual | Sole trader/small business |

|---|---|---|

| Proof of ID | Required | Required |

| Bank statements | 3 to 6 months | 3 to 6 months |

| Proof of income | Payslips or benefits | Accounts or SA302 |

| Business registration | Not needed | Required |

| VAT details | Not needed | If VAT-registered |

For tips tailored to your situation, our guide on leasing with poor credit covers the process in detail, and our tips for small businesses offer sector-specific advice.

Pro Tip: Prepare a written summary of your upfront payment offer before your first conversation with a provider. Stating clearly that you're willing to pay three or more months upfront can shift the entire tone of the negotiation in your favour.

Step-by-step guide to negotiating car lease terms

With paperwork in hand, it's time to approach negotiations methodically.

Negotiating a lease when your credit isn't perfect requires a clear strategy. Here's a step-by-step process that works:

- Be transparent from the start. Tell the provider about your credit situation early. Trying to hide it wastes time and damages trust when the check comes back.

- Identify what's negotiable. Upfront payments, mileage allowances, excess mileage charges, vehicle age, and contract length are all areas where there's often room to move.

- Offer a higher deposit. As noted in higher upfront payments guidance, offering 3 to 12 months upfront significantly improves your approval odds.

- Choose a less costly vehicle. Opting for an older model or a lower-spec car reduces the lender's risk and your monthly payment.

- Request manual underwriting. If an automated system declines you, ask for a human review. Automated systems can't account for context; a real person can.

- Review the full contract. Before signing, check mileage caps, maintenance responsibilities, and early exit clauses carefully.

- Compare at least three providers. Don't accept the first offer. Use soft-check providers where possible to protect your score.

For those who are newly employed with bad credit, extra documentation such as an employment contract can support your application. Our short-term leasing tips and affordable vehicle leasing guides offer further practical advice.

Pro Tip: Always ask whether the provider uses manual underwriting as an option. This single question can open doors that an automated rejection closes.

"For short-term or flexible lease needs, accept that early exit is rarely cheap. Build your budget around completing the term, not leaving it early."

Common pitfalls and how to avoid them

Having followed the negotiation steps, it's vital to sidestep the issues that trip up many lessees.

Even well-prepared applicants can stumble on details they didn't anticipate. Here are the most common pitfalls and how to avoid them:

- Ignoring Benefit in Kind (BiK) tax. If you're a business driver using a leased vehicle for personal journeys, HMRC will charge BiK tax. This can significantly increase your real cost. Always calculate BiK before committing to a BCH agreement.

- Underestimating early exit costs. Many people assume flexibility means they can leave a contract easily. In reality, early termination fees can be substantial. Read every clause.

- Overlooking mileage terms. Excess mileage charges can add up fast. Be realistic about how much you drive and negotiate a mileage cap that reflects your actual usage.

- Assuming a large deposit removes the credit check. A bigger upfront payment improves your odds, but most providers will still run some form of credit assessment.

- Skipping the small print on maintenance. Some leases include maintenance; others don't. Knowing who is responsible for tyres, servicing, and repairs avoids nasty surprises.

For BCH expert advice, the key nuance is that personal use of a business lease vehicle triggers BiK tax, which can erode the tax efficiency of the arrangement. Understanding personal leasing flexibility versus BCH terms is essential for small business owners.

"Short-term leasing suits those on probation or with seasonal needs, but if you need to exit early, flexibility is limited and it won't be cheap."

Our guide on flexible leasing for new businesses covers these trade-offs in more detail.

What success looks like: outcomes and next steps

With potential pitfalls covered, it's important to gauge your success and plan what comes next.

A fair lease deal for someone with bad or limited credit will look different from a standard prime-credit agreement, but it should still feel manageable and transparent. Here's what reasonable terms typically look like:

| Factor | Standard credit | Bad or limited credit |

|---|---|---|

| Upfront payment | 1 to 3 months | 3 to 12 months |

| Monthly rate | Market rate | 10 to 30% above market |

| Contract length | 24 to 48 months | 6 to 24 months |

| Mileage cap | Flexible | Fixed, often lower |

If your negotiated deal falls within these ranges, you're in a reasonable position. The goal isn't to match prime-credit terms; it's to get a workable agreement that fits your budget and timeline.

One reassuring fact: providers who specialise in this space report strong approval rates. An 88% approval rate for bad credit leasing applications is achievable when applicants are well-prepared and approach the right providers.

If negotiations fail with one provider, don't give up. Try a specialist bad credit lender, consider a lease takeover, or revisit your deposit offer. Our guide on leasing commercial vehicles is a useful next step if you need a van or commercial vehicle specifically.

Always review your agreement after signing. Set reminders for your contract end date so you can plan your next steps well in advance, whether that's renewing, returning the vehicle, or switching provider.

Our take: why flexibility in negotiation beats chasing the lowest price

Now, let's take a moment to view negotiation strategy from a broader perspective, shaped by experience in the UK market.

We've seen it many times. A customer pushes hard for the lowest possible monthly payment, wins that battle, and then finds themselves locked into rigid terms that cost far more when life changes. For people with bad credit or small businesses managing cash flow, that trade-off is particularly painful.

The truth is, a slightly higher monthly rate paired with genuine flexibility is almost always the better deal. Providers who feel respected and dealt with honestly are far more likely to accommodate a request to adjust mileage, extend a contract, or work with you if payments become difficult.

Aggressive price negotiation can signal desperation or risk to a provider, which tightens their terms rather than loosening them. Building a relationship, being open about your situation, and showing you've done your homework creates goodwill that pays dividends throughout the contract.

For real-world short-term lease advice, the consistent theme is that customers who prioritise flexibility and communication get better overall outcomes than those who focus solely on price. A marginal saving on your monthly payment is rarely worth sacrificing the ability to adapt when you need to.

Ready to negotiate your next flexible lease?

If you're considering your own leasing journey, here's where to get expert help and tailored options.

At Flexi Auto Lease, we specialise in helping individuals and small business owners across the UK access flexible vehicle leasing, regardless of credit history. Our process uses soft or no credit checks, so exploring your options won't affect your credit score.

We offer short-term lease options from 6 to 24 months, covering private cars, SUVs, electric vehicles, and commercial vans. Pricing is all-inclusive, covering road tax and maintenance, with nationwide delivery available. Whether you have bad credit, limited credit, or you're newly self-employed, we're here to help you find a deal that works. Browse our stock today and get approved in days, not weeks.

Frequently asked questions

Will negotiating a car lease hurt my credit score?

Negotiating itself doesn't affect your score, but a hard credit check during the application process might show on your report. Choosing providers who use soft checks, as noted in manual underwriting options, helps protect your score.

Can I get a short-term lease if I'm newly employed?

Yes, many lessors consider newly employed applicants with extra documentation or a larger deposit. Providing your employment contract alongside standard documents, as outlined in extra documentation guidance, can significantly strengthen your application.

Is a higher deposit always required for bad credit?

A bigger upfront payment is common for bad credit, but some providers offer low-deposit options. Deposits of 3 to 12 months are typical, but terms vary, so always check before applying.

Can I reclaim VAT if I lease as a business?

If your business is VAT-registered and the lease qualifies, you can reclaim 50 to 100% of the VAT portion. BCH is tax deductible and VAT reclaimable for eligible businesses, making it a cost-efficient option.

What's the easiest way to pass a lease check with bad or thin credit?

Prepare comprehensive documents, offer a higher deposit, and consider a cheaper car or a guarantor. Better documentation and deposit strategies consistently improve approval outcomes for applicants with limited or poor credit histories.