Getting a car on a short-term lease when your credit history is less than perfect can feel like hitting a wall. Many people across the UK face this exact frustration, whether they are self-employed, newly employed, or simply carrying the weight of past financial difficulties. The good news is that specialist providers now offer genuinely flexible auto lease options for terms of 6 to 24 months, and some do not require a hard credit check at all. This guide walks you through every stage of the process, from understanding your options to collecting your keys, so you can move forward with confidence.

Table of Contents

- Understanding flexible auto leasing in the UK

- What you need before you start: requirements and preparation

- Step-by-step workflow for a flexible auto lease

- Troubleshooting and common mistakes to avoid

- What to expect: results, handover, and aftercare

- Get started with a flexible auto lease that fits your needs

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Flexible leasing options exist | Even with bad credit, you can access flexible short-term car leases using specialist providers. |

| Preparation boosts success | Gathering the right documents and choosing affordable options increase your chance of approval. |

| Affordability matters more than credit | Many providers focus on income and affordability, not just your credit score. |

| Short terms mean higher cost | Expect to pay more per month for the benefit of short lease durations and flexibility. |

Understanding flexible auto leasing in the UK

Flexible auto leasing means you can access a vehicle without committing to a long, rigid contract. Instead of a traditional three to five year agreement, you choose a term that suits your situation, typically anywhere from 6 to 24 months. You also get to agree on a mileage allowance upfront, and some arrangements allow early exit without heavy penalties.

There are three main car lease types to know about:

- Personal Contract Hire (PCH): Designed for individuals. You pay a fixed monthly amount and return the car at the end.

- Business Contract Hire (BCH): Aimed at limited companies and sole traders. As noted in business leasing details, BCH allows eligible businesses to reclaim VAT and benefit from tax relief, making it more cost-effective.

- Flexible subscriptions: A newer model where you pay monthly with rolling terms. These are often all-inclusive, covering road tax and maintenance.

The flexible contract lengths available today mean you are not locked in unnecessarily. However, 6-24 month leasing typically costs more per month than a long-term deal because the provider carries more risk over a shorter period.

"Flexible auto leasing in the UK for 6 to 24 months uses PCH for individuals or BCH for small businesses, but true no-impact options are rare and rely on affordability over credit history rather than a traditional credit score."

If your credit score is low or limited, standard high-street leasing companies will often decline your application outright. Specialist providers take a different approach, focusing on whether you can afford the monthly payments rather than penalising you for past difficulties. That shift in focus opens the door for a much wider range of applicants.

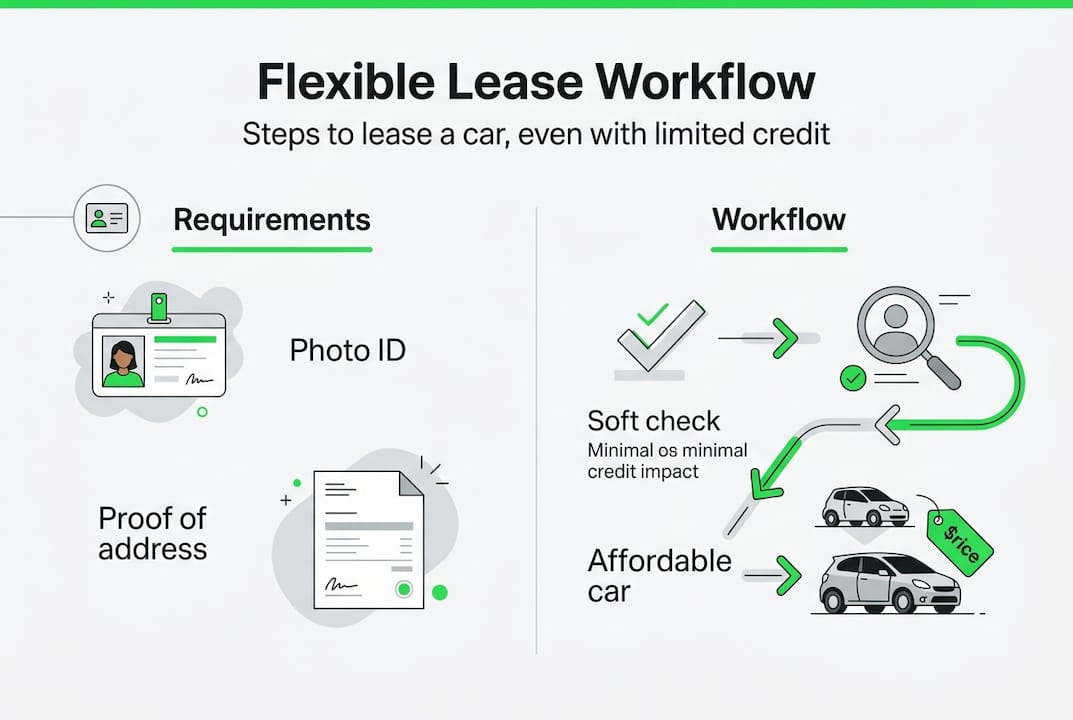

What you need before you start: requirements and preparation

With an understanding of the different types of flexible leases and their credit implications, you can now get prepared. Being organised before you apply makes a real difference, especially when your credit history is not straightforward.

Here is a comparison of typical requirements for individuals versus small businesses:

| Requirement | Individual applicant | Small business applicant |

|---|---|---|

| Photo ID | Passport or driving licence | Director's passport or driving licence |

| Proof of address | Utility bill or bank statement | Registered business address proof |

| Proof of income | Payslips or bank statements | Business accounts or tax returns |

| Business documents | Not required | Company registration, VAT number |

| Credit or affordability check | Affordability assessment | Affordability and business viability check |

The standard application workflow includes vehicle selection, choosing your duration and mileage, submitting documents and proof of income, and then an affordability and credit review. Having everything ready speeds this up considerably.

Documents you will typically need:

- Valid photo ID (passport or driving licence)

- Two recent proof of address documents

- Three months of bank statements or payslips

- If self-employed: two years of accounts or an SA302 tax summary

- If a limited company: Companies House registration number and recent accounts

Our car lease checklist covers everything in detail, and our guide on leasing with limited credit explains how affordability assessments work in practice.

Pro Tip: Choose a vehicle that sits comfortably within your budget rather than stretching for a premium model. Providers are far more likely to approve applications where the monthly payment represents a realistic proportion of your income.

Step-by-step workflow for a flexible auto lease

After gathering your paperwork, you are ready to move through the workflow. Here is exactly what each step looks like, so there are no surprises along the way.

- Browse and select your vehicle. Choose a car that fits your budget and practical needs. Smaller, more affordable vehicles improve your approval odds if your credit is limited.

- Choose your lease terms. Decide on your contract length (6 to 24 months) and your estimated annual mileage. Underestimating mileage leads to excess charges, so be realistic.

- Submit your application and documents. Provide all required ID, income proof, and business documents where applicable. The full workflow covers vehicle selection through to delivery.

- Affordability assessment. With specialist providers, affordability rather than hard credit is the primary measure. This means no hard footprint on your credit file.

- Pay your initial rental. This is typically one to three months upfront. A higher initial payment can improve your chances of approval.

- Sign your contract. Review the flexible lease terms carefully before signing, paying attention to mileage limits and wear and tear conditions.

- Vehicle delivery. Many providers offer nationwide delivery directly to your door, often within a few days of approval.

- Monthly payments begin. Payments are fixed for the duration of your contract, making budgeting straightforward.

Here is how the standard and specialist provider workflows compare:

| Stage | Standard provider | Specialist provider |

|---|---|---|

| Credit check | Hard credit check | Soft or no credit check |

| Approval basis | Credit score focused | Affordability focused |

| Approval speed | Several days to weeks | Often within 24 to 48 hours |

| Deposit requirement | Standard initial rental | May accept higher initial rental |

| Flexibility | Fixed terms only | Rolling and fixed terms available |

For those starting a new venture, our guide on leasing for new businesses is particularly useful. You can also explore Fleet Evolution options for a broader view of what short-term business leasing looks like in practice.

Pro Tip: Offering a higher initial rental payment, such as three months upfront instead of one, signals financial commitment to the provider and can significantly improve your chances of approval when your credit history is limited.

Troubleshooting and common mistakes to avoid

Even with the perfect plan, things can go wrong. Here is how to avoid the most common pitfalls and tackle application setbacks before they derail your plans.

Common mistakes and how to handle them:

- Applying for a vehicle above your means. Providers assess affordability carefully. If the monthly payment is too high relative to your income, your application will be declined. Choosing a less expensive vehicle or offering a higher deposit improves your position considerably.

- Incomplete or inconsistent documents. Missing payslips or mismatched addresses on ID and bank statements cause delays or outright rejections. Double-check everything before submitting.

- Underestimating mileage. Excess mileage charges at the end of a lease can be costly. Always estimate slightly higher than you think you will need.

- Not reading the contract terms. Many applicants skip the small print and are surprised by end-of-lease charges.

- Applying with multiple providers simultaneously. If each provider runs a hard credit check, multiple applications in a short period can damage your score further. Stick to specialist providers who use soft checks.

If you are in new employment, some providers will still consider your application if you can show a signed employment contract alongside recent bank statements.

"Always read the wear and tear guidelines in your lease agreement before you drive away. Returning a vehicle with damage beyond fair wear and tear can result in unexpected charges that catch many lessees off guard at the end of their contract."

What to expect: results, handover, and aftercare

With the application complete, here is what happens next so you can take control and avoid last-minute headaches.

At handover, check the following:

- The vehicle condition report matches the actual state of the car

- All keys, documents, and accessories are present

- You understand the mileage limit and any fair wear and tear guidelines

- You have the provider's contact details for support

During your lease, your routine tasks include:

- Making monthly payments on time to avoid penalties

- Keeping within your agreed mileage allowance

- Arranging servicing as required (many all-inclusive leases cover this)

- Reporting any damage or mechanical issues promptly

Flexible leasing is now firmly mainstream. 2.5 million UK business vehicle leases were recorded in 2024, up 8% year on year, showing just how many businesses and individuals are choosing this route. It is worth comparing leasing vs hire purchase if you are unsure which suits your longer-term needs.

At the end of your lease, you typically have three options:

- Return the vehicle and walk away

- Renew with the same or a different vehicle

- Request an extension if your circumstances have changed

Planning ahead for the end of your contract avoids any last-minute scramble and keeps your options open.

Get started with a flexible auto lease that fits your needs

Now you know what to expect from application to aftercare, you are ready to find out how easy it can be to get started with the right provider. Whether you are an individual looking for a reliable car without the credit stress, or a small business owner needing a flexible van or company vehicle, the right support makes all the difference.

At Flexi Auto Lease, we make the process straightforward. Our flexible car leasing options cover a wide range of vehicles, from everyday hatchbacks to SUVs, electric vehicles, and commercial vans. We use soft credit checks so your credit score is never affected by simply applying. Nationwide delivery means you could be driving within days of approval. Browse our stock, apply online, and let us handle the rest. We are here to help you get moving, whatever your credit history looks like.

Frequently asked questions

Can I really get a short-term car lease in the UK with bad credit?

Yes, specialist providers use affordability assessments rather than a hard credit check, making approval genuinely possible even if your credit history is poor or limited.

Do I need to provide a high deposit for a flexible lease?

Not always. While offering a higher initial rental can improve your approval chances, affordable options with lower upfront costs are available if you can clearly demonstrate a steady income.

What documents are required for a 6 to 24 month flexible lease?

You will typically need valid photo ID, proof of address, recent bank statements or payslips, and if applying as a business, your company registration details and accounts.

Is there a difference between PCH and BCH for flexible leasing?

Yes. PCH is designed for private individuals, while BCH is for businesses and allows eligible companies to reclaim VAT and benefit from tax relief, making it the more cost-effective route if you qualify.