Bad credit does not have to mean no car. Many people assume that a poor or limited credit history puts vehicle leasing completely out of reach, but that simply is not true. Flexible leasing contracts have changed the landscape, making it possible for individuals and small business owners across the UK to get behind the wheel without the stress of rigid agreements or strict credit score requirements. This guide explains exactly what contract flexibility means, how it helps those with credit challenges, and what to look for before you sign up.

Table of Contents

- What does contract flexibility in leasing mean?

- How flexible leasing helps those with bad or limited credit

- Types of contract flexibility and real-life examples

- What to consider before choosing a flexible lease

- Why contract flexibility is more than marketing: Our view

- Take the next step with flexible leasing options

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Lease flexibility explained | Flexible contracts let you adapt vehicle leasing terms to suit financial needs, especially helpful with bad credit. |

| Access for bad credit | Shorter, adaptable leases make approval easier and reduce barriers for those with limited credit history. |

| Practical options available | Larger deposits, affordable cars, and honest communication boost your chances of a flexible lease. |

| Read terms carefully | Always review fees and conditions before signing to avoid common pitfalls. |

What does contract flexibility in leasing mean?

Contract flexibility in vehicle leasing refers to your ability to adjust key aspects of your lease agreement without facing heavy penalties. In a traditional lease, you are locked into fixed terms from day one. Change your mileage, end the contract early, or swap the vehicle, and you could face significant charges. A flexible lease works differently. It gives you room to adapt.

The main types of flexibility you will find in leasing include:

- Contract length: Choose shorter terms, often between 6 and 24 months, rather than being tied in for three or four years.

- Mileage adjustments: Some providers allow you to revise your agreed annual mileage if your circumstances change.

- Vehicle swapping: Upgrade, downgrade, or switch to a different model during or at the end of your term.

- Early exit options: Leave the contract before the end date, sometimes with little or no penalty, depending on the provider.

For anyone with bad or limited credit, these features are genuinely valuable. Standard leasing companies often rely heavily on credit scores to assess risk. Flexible leasing specialists take a broader view. They look at your current affordability, your employment situation, and the value of the vehicle itself. As specialist leasing companies focus on affordability and short terms, contract flexibility becomes accessible even for those with a difficult credit history.

"Flexible leasing is not just about convenience. For people rebuilding their finances, it can be a genuinely practical route back to reliable transport."

Understanding flexible lease terms before you apply helps you ask the right questions and avoid surprises. It is also worth reading up on leasing flexibility explained so you know exactly what rights and options you hold throughout the agreement.

The core difference between a typical contract and a flexible one comes down to control. With a fixed contract, the lender holds most of it. With a flexible contract, you share it.

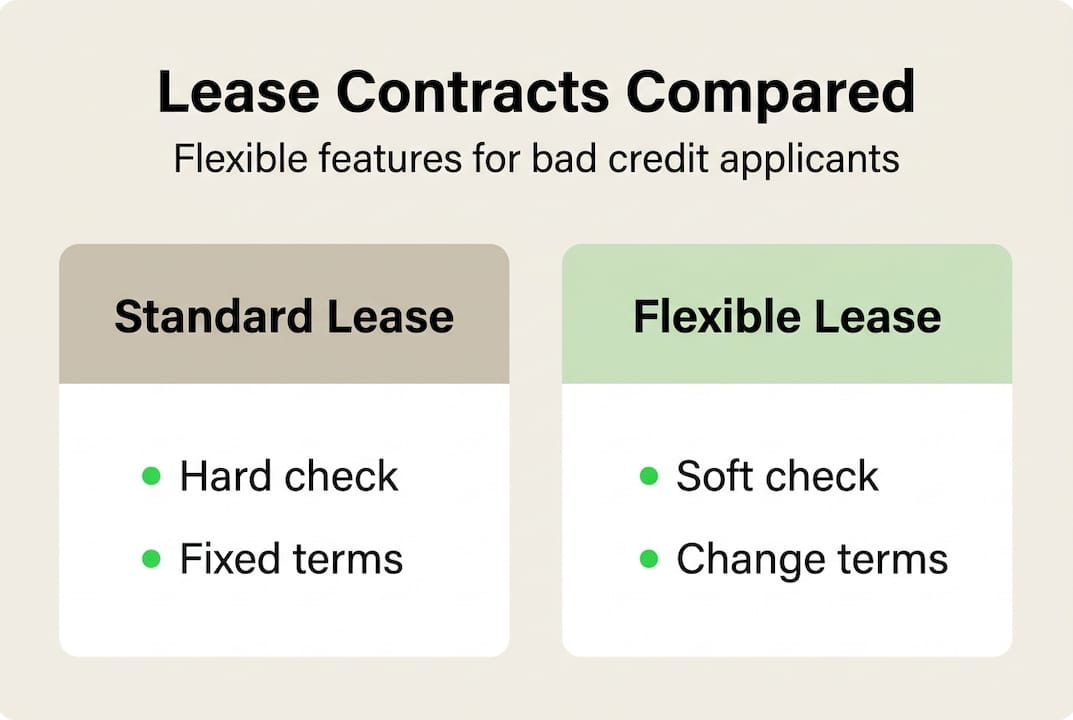

How flexible leasing helps those with bad or limited credit

Flexible leasing removes some of the biggest barriers that people with adverse credit profiles face. Traditional lenders focus almost entirely on your credit score. Flexible leasing specialists take a different approach. They assess your current income, your outgoings, and whether the monthly payments are genuinely manageable for you.

Here is a quick comparison of what you might expect:

| Feature | Standard lease | Flexible lease |

|---|---|---|

| Credit check type | Hard check | Soft or no check |

| Contract length | 24 to 48 months | 6 to 24 months |

| Deposit required | 1 to 3 months | Sometimes higher |

| Early exit option | Rarely | Often available |

| Approval speed | Slower | Often within days |

Shorter contract terms are particularly helpful. Short-term contracts are less risky for lenders and more accessible to those with poor or limited credit, which means approval rates are generally higher. The lender's exposure is reduced, so they can afford to be more accommodating.

Common requirements you may encounter include:

- A higher initial payment or deposit

- A guarantor, particularly if your credit history is very limited

- Choosing a lower-cost or more practical vehicle model

- Proof of income or employment, including self-employment records

Some providers only carry out a soft credit check, meaning the search does not appear on your credit file and will not affect your score. This is a significant advantage if you are already concerned about your credit rating. You can explore the short-term leasing benefits in more detail, and if you are just starting to build a credit history, reading about leasing with limited credit can give you a clearer picture of what to expect.

Pro Tip: Be upfront with your leasing provider about your financial situation. Honest communication about your income, outgoings, and credit history actually increases your chances of approval. Providers can tailor the agreement to suit your circumstances rather than offering a one-size-fits-all solution.

Types of contract flexibility and real-life examples

Let us look at how contract flexibility plays out in practice, particularly for UK individuals and small business owners.

Fixed vs. flexible leasing at a glance:

| Aspect | Fixed contract | Flexible contract |

|---|---|---|

| Term changes | Not permitted | Often allowed |

| Mileage changes | Charged at end | Adjustable mid-term |

| Vehicle swap | Not available | Available with some providers |

| Early termination | Heavy penalties | Reduced or no penalties |

| Suitable for bad credit | Rarely | Yes, with specialist providers |

Here are some everyday scenarios where flexibility makes a real difference:

- Vehicle swap: A sole trader leases a small hatchback but wins a new contract requiring a van. A flexible agreement allows them to swap vehicles without losing money or breaking the contract.

- Adjusting contract length: A newly employed professional takes a 6-month lease while their probation period is underway. Once confirmed in post, they extend to 12 months without starting a new application.

- Changing mileage mid-term: A small business owner underestimates their monthly mileage. Rather than paying excess charges at the end, they adjust the agreed mileage during the contract.

- Early exit: A self-employed individual experiences a slow trading period and needs to reduce costs. A flexible contract allows them to hand back the vehicle without a crippling penalty.

For those with limited credit, larger deposits and affordable cars are practical strategies that help secure flexible contracts. Choosing a vehicle with lower monthly payments reduces the lender's risk and makes approval far more likely.

If you run a small business, exploring flexible leasing tips for small businesses can help you make the most of these options. There is also useful guidance on SME leasing term options if you need a structure that fits around your trading patterns.

What to consider before choosing a flexible lease

Flexible leasing is a strong option for many people, but it is important to go in with your eyes open. Before you sign anything, ask your provider these key questions:

- Are there any fees for changing the contract length or mileage?

- What are the exact terms for early termination?

- Is the initial payment refundable if circumstances change?

- Does the agreement include maintenance, road tax, and breakdown cover?

- What happens if I miss a payment?

Common pitfalls to avoid include:

- Unclear terms: Always read the small print. If a provider is vague about flexibility clauses, ask for written clarification before signing.

- Overestimating mileage: Choosing a higher mileage allowance to feel safe can push up your monthly payments unnecessarily. Be realistic.

- Ignoring upfront costs: Opting for a more affordable vehicle and being prepared for larger deposits can genuinely boost your acceptance chances, but make sure you have those funds available before applying.

Who benefits most from contract flexibility? In short, anyone whose circumstances are likely to change. That includes newly employed workers, self-employed individuals with variable income, small business owners managing seasonal demand, and anyone actively working to improve their credit score.

For practical guidance, our short-term leasing tips cover the key things to watch for. If budget is a priority, affordable vehicle leasing gives you a clear framework for keeping costs manageable. And if you have recently started a new job, our guide on leasing when newly employed is worth a read.

Pro Tip: Always compare the total cost of the lease, not just the monthly payment. Add up the initial payment, all monthly instalments, and any end-of-contract fees to get the real picture. And have a backup plan in case your credit situation changes during the term.

Why contract flexibility is more than marketing: Our view

We have seen a lot of providers use the word "flexible" as a selling point without really meaning it. Hidden conditions, vague clauses, and unexpected fees can turn a supposedly flexible contract into something that feels very rigid once you are in it. True flexibility means transparency, and that is something we take seriously.

From our experience, the customers who succeed with flexible leasing are the ones who go in prepared. They understand the upfront costs, they provide honest documentation, and they choose a vehicle that genuinely fits their budget. When those things are in place, approval rates rise significantly.

We also believe that flexible leasing can be a real stepping stone to better credit, but only if the contract terms are clear and support change rather than punish it. A well-structured flexible contract length gives you the breathing room to manage your finances without the fear of being trapped. That is what genuine flexibility looks like.

Take the next step with flexible leasing options

If you have been held back by concerns about your credit history, it is time to see what is actually possible. Flexible contracts put decision-making back in your hands, giving you the ability to choose terms that suit your life rather than the other way around.

At Flexi Auto Lease, we work with individuals and small businesses across the UK to find flexible lease options that fit your budget and your circumstances. Whether your credit is limited, patchy, or a work in progress, we are here to help you find a plan that works. Browse our vehicles, apply in minutes, and you could be driving within days. No hard credit checks. No unnecessary stress. Just straightforward, accessible leasing designed around you.

Frequently asked questions

Can I get a car lease with bad or no credit in the UK?

Yes, specialist leasing providers focus on affordability and shorter contract terms rather than strict credit scores, making flexible leasing accessible even with a poor or limited credit history.

What strategies can help me secure a flexible lease agreement with poor credit?

Offering a larger deposit, guarantor, or choosing a more affordable vehicle are the most effective ways to improve your chances of approval with a flexible lease.

Are there flexible lease options for small businesses with limited trading history?

Short-term flexible contracts lower the lender's risk, making them a practical option for new or small businesses that do not yet have a long credit or trading history.

Will I face higher costs for choosing a flexible contract due to my credit profile?

You may be asked for a higher initial payment or slightly higher monthly rate, but these terms improve acceptance chances and are often worth the trade-off for the flexibility you gain.

Can I end my lease early or change terms later with a flexible contract?

Most flexible contracts do allow early exit or term changes, but always check the specific conditions and any associated fees before you sign.