Car leasing is no longer the exclusive territory of large corporations with spotless credit files and years of trading history behind them. If you run a small or medium-sized business in the UK, flexible leasing options are very much within your reach, even if your credit history is limited or your business is relatively new. Yet many SME owners still feel put off by unfamiliar jargon and complex-looking agreements. This guide cuts through the confusion, explains the key terms in plain English, and helps you make confident, informed decisions about leasing a vehicle for your business.

Table of Contents

- What does car leasing mean for UK SMEs?

- Key car leasing terms explained

- Types of car leases: which one fits your SME?

- What SMEs need to qualify for a car lease

- Costs, fees and tax breaks: what you pay and what you save

- Common pitfalls and expert strategies for SME leasing

- Explore flexible car leasing solutions for your SME

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Leasing supports flexibility | SMEs can avoid ownership hassles and upgrade vehicles with fixed monthly costs. |

| Eligibility is clear but flexible | Most UK SMEs qualify if they are registered and trading for 1-2 years, though startups have options too. |

| Mind term details | Key terms like mileage allowance, deposits, and contract length dictate real costs. |

| Tax savings available | Leasing may offer VAT recovery and benefit-in-kind advantages, especially for electric vehicles. |

| Watch for extra fees | Excess mileage, early termination, and wear charges can add up if not managed proactively. |

What does car leasing mean for UK SMEs?

Business car leasing is essentially a long-term rental arrangement. You pay a fixed monthly amount to use a vehicle, and at the end of the contract, you hand it back. You never own the car, but you always have access to a reliable, up-to-date vehicle without the large upfront cost of buying outright.

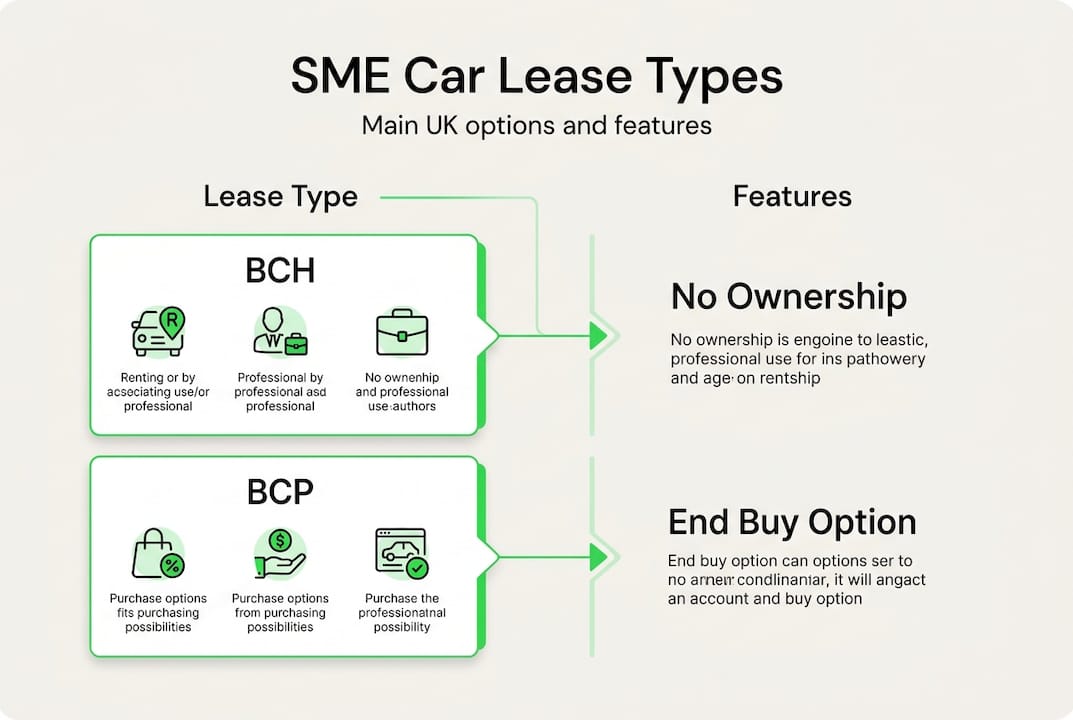

Business Contract Hire (BCH) is the most popular leasing model for UK SMEs. It offers predictable monthly payments, no ownership risk, and the option to upgrade at the end of the term. Other options include Business Contract Purchase (BCP), Lease Purchase, and Finance Lease, each with slightly different structures depending on whether ownership matters to your business. You can explore the full range of UK car lease types to find the right fit.

Here are the core terms you will encounter in any leasing arrangement:

- Lessor: The leasing company that owns the vehicle and provides it to you.

- Lessee: Your business, which uses the vehicle under the agreed terms.

- Contract length: Typically 24 to 48 months, though shorter terms are available.

- Monthly rental: Your fixed payment, covering depreciation and interest.

- Mileage allowance: The maximum miles agreed per year in your contract.

"Understanding the business leasing basics before you sign is the single most effective way to avoid unexpected costs and get genuine value from your agreement."

Leasing is structured to support cashflow. Rather than tying up capital in a depreciating asset, you preserve working capital and keep your monthly outgoings predictable.

Key car leasing terms explained

Now that you have the overall landscape, let us break down the actual language you will see on a leasing agreement and what each term means for your business.

Fixed monthly rentals cover depreciation to around 75% of the car's value, plus interest at 4 to 9% APR, with typical agreements running 24 to 48 months and 8,000 to 12,000 miles per year. Knowing this helps you budget accurately and compare offers on a like-for-like basis.

| Term | What it means | Why it matters |

|---|---|---|

| Initial deposit | Upfront payment, usually 3 to 9 monthly rentals | Affects your starting cashflow |

| Monthly rental | Fixed payment covering depreciation and interest | Core budgeting figure |

| Contract length | Duration of the lease, typically 24 to 48 months | Longer terms often mean lower monthly costs |

| Mileage allowance | Agreed annual mileage cap | Exceeding this triggers extra charges |

| Excess mileage | Per-mile charge above your allowance | Can add up quickly if underestimated |

| APR | Annual Percentage Rate, the cost of borrowing | Helps compare deals accurately |

| Wear and tear | Acceptable condition standards at return | Damage beyond this incurs charges |

Pro Tip: Before signing, ask the leasing provider for a written definition of their wear and tear standards. Different providers apply different thresholds, and knowing this upfront protects you at the end of the contract.

For more practical guidance, our car leasing tips for small businesses and our leasing explained for startups guide are both worth reading alongside this article.

Types of car leases: which one fits your SME?

With the meanings of all key terms now clear, it is time to see how those terms play out across the different lease types available to SMEs.

BCH means no ownership at the end of the contract, with the option to return or upgrade the vehicle. BCP, Lease Purchase, and Finance Lease each offer varying degrees of ownership potential and flexibility. Choosing the right type depends on your priorities around cashflow, ownership, and flexibility.

| Lease type | Ownership at end | Best for | Key consideration |

|---|---|---|---|

| Business Contract Hire (BCH) | No | Cashflow-focused SMEs | Lowest monthly cost, no asset |

| Business Contract Purchase (BCP) | Optional | SMEs wanting flexibility | Option to buy at end |

| Lease Purchase | Yes | SMEs planning ownership | Higher monthly payments |

| Finance Lease | Possible via sale | Asset-conscious businesses | Off-balance-sheet option |

Here is a quick summary of what to weigh up:

- Mileage limits are fixed in BCH and BCP. Exceeding them is costly.

- Early termination fees can be significant across all types. Check these before signing.

- Deposits vary. A larger initial payment usually reduces monthly costs.

- Ownership preference is the clearest deciding factor between BCH and the other types.

For SMEs with short-term needs or limited credit, short-term lease options can offer real flexibility. It is also worth comparing leasing vs hire purchase if ownership is a priority. The AA also provides a useful breakdown of BCH versus purchase for UK businesses.

What SMEs need to qualify for a car lease

Having explored the main contract types, let us clarify what your business needs to put in place in order to qualify for a car lease.

Eligibility for SMEs is based on UK registration as a sole trader, partnership, or limited company, generally with one to two years of trading history. Startups can still apply, but may face stricter checks and conditions. Credit checks on both the business and its directors are standard practice.

Here is a straightforward checklist to prepare your application:

- Proof of business registration: Companies House number or sole trader registration.

- Trading history: At least 12 months of bank statements or accounts where possible.

- VAT certificate: If your business is VAT-registered.

- Directors' details: Personal information for credit checks.

- Proof of address: For both the business and individual directors.

- Financial statements: Recent profit and loss accounts or tax returns.

Pro Tip: If your business is new or has limited credit, consider offering a larger initial deposit. This reduces the lender's risk and significantly improves your chances of approval.

Our guides on leasing for new businesses and leasing with limited credit offer further practical steps if your situation is less straightforward.

Costs, fees and tax breaks: what you pay and what you save

Once you understand how to qualify, it is crucial to get a clear picture of what a lease will actually cost and where the potential savings lie.

Monthly rentals for SMEs typically range from £277 to £400 plus VAT, with initial deposits around £1,600 to £2,000. Excess mileage charges average 8.9p per mile. VAT-registered SMEs can reclaim 50 to 100% of VAT on rentals, and electric vehicles attract a Benefit-in-Kind (BiK) rate as low as 3% in 2026.

| Cost or saving | Typical figure | Notes |

|---|---|---|

| Monthly rental | £277 to £400 plus VAT | Varies by vehicle and term |

| Initial deposit | £1,600 to £2,000 | Usually 3 to 9 monthly rentals |

| Excess mileage charge | 8.9p per mile plus VAT | Applies above contracted allowance |

| VAT reclaim | 50 to 100% | Depends on business use percentage |

| EV BiK rate | From 3% | Significant saving versus petrol or diesel |

Watch out for these potential extras:

- Early termination fees: These can be substantial, sometimes equivalent to several months of rentals.

- Wear and tear charges: Damage beyond the agreed standard is charged at the end of the contract.

- Admin fees: Some providers charge for processing, documentation, or vehicle collection.

If your business is considering an electric vehicle, the EV leasing tax breaks available in 2026 make this an especially attractive option. The MINI Cooper Electric is one example of a popular business EV lease choice.

Common pitfalls and expert strategies for SME leasing

With costs and eligibility covered, here is what most SMEs miss: the small print, hidden costs, and the tactics that can make a real difference to your leasing experience.

Early termination can be costly, excess mileage charges of 8.9p per mile or higher apply above your allowance, end-of-lease wear and tear is tightly defined, and BCH agreements include no ownership at the end. These are the four areas where SMEs most commonly encounter unexpected costs.

Here is how to protect yourself:

- Estimate your mileage honestly. Underestimating to get a lower monthly payment almost always costs more in the long run.

- Read the wear and tear guidelines before you take delivery, not just at the end.

- Clarify early exit terms in writing before signing. Business needs change, and you need to know the cost of flexibility.

- Review business versus personal use. If employees use the vehicle privately, this triggers additional BiK tax liability.

- Negotiate contract length and mileage to match your actual needs rather than accepting standard terms.

"The businesses that get the most from leasing are those that treat the agreement as a financial tool, not just a vehicle arrangement. Plan your mileage, understand your exit options, and review the full terms before you commit."

For SMEs managing multiple vehicles, our fleet flexibility tips offer practical strategies to keep costs under control as your business grows.

Explore flexible car leasing solutions for your SME

You now have a solid understanding of car leasing terms, costs, and strategies. The next step is finding a provider that genuinely works for your business, whatever stage you are at.

At Flexi Auto Lease, we offer flexible car leases for SMEs across the UK, with options designed for businesses at every stage, including those with limited credit or short trading histories. Our process is straightforward: browse our vehicles, apply online, and drive within days. We support sole traders, partnerships, and limited companies, and we specialise in helping businesses that have been turned away elsewhere. If you are exploring SME leasing for bad credit, we have tailored solutions ready for you. Get in touch today and let us find the right vehicle for your business.

Frequently asked questions

What documents do SMEs need to provide for a car lease application?

Typically, you will need proof of business trading such as accounts or bank statements, company registration details, a VAT certificate if applicable, and directors' details for credit checks. Having these ready speeds up the approval process considerably.

Can a new SME with limited credit still lease a car?

Yes, some providers will consider startups with limited credit, though you may need to provide additional documentation or a larger initial deposit to secure approval.

Are maintenance and insurance included in SME lease agreements?

Monthly rentals cover depreciation only as standard, but maintenance packages can often be added. Insurance is almost always arranged separately by the business.

What happens if my SME exceeds the mileage allowance?

You will be charged a per-mile fee for every mile above your contracted limit. Excess mileage fees for UK business car leasing average 8.9p plus VAT per mile, so accurate mileage planning is essential.

Can I reclaim VAT on business car lease payments?

VAT-registered SMEs can reclaim 50 to 100% of VAT on lease rentals, depending on the proportion of business-only use and the type of vehicle leased.