Contrary to popular belief, leasing a car doesn't always involve a hard credit check that damages your score. All inclusive car leasing in the UK bundles road tax, maintenance, and breakdown cover into one fixed monthly payment, making it an accessible and transparent option for individuals and small businesses with bad or limited credit who need reliable, flexible transport without the financial uncertainty of traditional vehicle finance.

Table of Contents

- Introduction To All Inclusive Car Leasing

- How All Inclusive Leasing Works For Bad Credit Or Limited Credit

- What All Inclusive Car Leasing Covers: Transparency And Cost Savings

- Common Misconceptions About Leasing With Bad Credit

- Comparison Of All Inclusive Leasing Vs Traditional Vehicle Finance For Bad Credit

- Practical Steps To Lease A Car With Bad Credit In The UK

- Benefits Of All Inclusive Leasing For Individuals And Small Businesses

- Discover Flexible All Inclusive Car Leasing Options Today

- Frequently Asked Questions

Key takeaways

| Point | Details |

|---|---|

| Bundled costs | All inclusive leases combine road tax, maintenance, warranty, and breakdown cover into fixed monthly payments. |

| Credit-friendly | Soft or no credit checks prevent negative impacts on your credit score. |

| Flexible terms | Short-term leases from 6 to 24 months suit changing personal or business needs. |

| Lower deposits | Many providers offer zero or reduced deposits compared to traditional finance. |

| Budget clarity | Fixed payments eliminate unexpected vehicle expenses, making financial planning easier. |

Introduction to all inclusive car leasing

All inclusive car leasing is a UK vehicle rental model where your monthly fee covers road tax, servicing, warranty, and breakdown assistance alongside the car itself. Unlike traditional leasing or hire purchase, you pay one predictable amount each month without juggling separate bills for maintenance or tax. This approach delivers budgeting certainty and reduces the risk of surprise costs that can derail your finances. However, all inclusive car leasing packages typically exclude vehicle fuel costs and any damage beyond normal wear and tear, which you must plan for separately.

For individuals and small businesses facing credit challenges, this model offers reliable transport without the barriers of traditional finance. Self-employed workers, new employees, and those rebuilding credit find all inclusive leasing particularly valuable because it addresses their need for flexible, affordable mobility. The bundled services mean less administrative hassle and fewer hidden fees, making it easier to forecast your monthly outgoings accurately. In many ways, all inclusive leasing mirrors the convenience found in other sectors, such as all inclusive ski transfer perks that simplify travel logistics.

Key features of all inclusive car leasing include:

- Road tax paid for the entire lease duration

- Regular servicing and maintenance covered by the provider

- Manufacturer warranty protecting against mechanical failures

- Breakdown assistance ensuring help when you need it

- Predictable monthly costs with no surprise bills

This structure contrasts sharply with standard leasing, where you separately arrange and pay for tax, maintenance, and cover, adding complexity and potential cost overruns.

How all inclusive leasing works for bad credit or limited credit

Many UK short-term and all inclusive leasing providers use soft credit checks or no credit checks to approve customers, avoiding hard inquiries that negatively impact credit scores. A soft check verifies your affordability and identity without leaving a mark on your credit report, whilst some providers skip credit checks entirely, relying instead on income verification, employment status, and occasionally guarantors. This approach opens doors for applicants with poor or limited credit histories who would struggle to secure traditional vehicle finance.

Deposits vary significantly but are often reduced or waived compared to conventional leasing or hire purchase agreements. Providers manage risk through shorter lease terms and bundled maintenance services, which prevent defaults caused by unexpected repair bills. By keeping contracts between 6 and 24 months, lessors limit their exposure whilst giving you the flexibility to adapt as your circumstances change. You'll typically need a valid UK driving licence, proof of income such as payslips or bank statements, and DVLA address confirmation to complete your application.

Pro Tip: Gather comprehensive income documents including recent bank statements, payslips, or tax returns before applying to improve your approval chances, especially if you have limited credit history or are self-employed.

Essential application requirements include:

- Valid UK driving licence with minimal penalty points

- Proof of stable income through employment or self-employment

- Current address verified via DVLA records or utility bills

- Age typically 21 or over, depending on the provider

- UK bank account for direct debit payments

By structuring agreements this way, all inclusive leasing providers make vehicle access realistic for people who might otherwise face rejection from traditional lenders.

What all inclusive car leasing covers: transparency and cost savings

Understanding exactly what your monthly payment includes helps you budget accurately and avoid unpleasant surprises. All inclusive leases bundle road tax, scheduled maintenance inspections, manufacturer warranty, and breakdown cover into your fixed monthly fee. These services typically account for a significant portion of vehicle running costs, so having them included simplifies your financial planning. However, all inclusive leasing packages typically exclude vehicle fuel costs and any damage beyond normal wear and tear, which remain your responsibility.

Excluded costs include fuel for all journeys, tyre replacements due to wear, repairs for damage exceeding normal use, and insurance excesses if applicable. Transparent fixed monthly payments reduce the risk of budget-busting bills for routine servicing or unexpected breakdowns. By knowing upfront what you'll pay each month, you can plan other expenses with confidence.

Pro Tip: Request a detailed written breakdown of all contract terms before signing to confirm exactly what services are included and identify any potential hidden fees or charges.

The table below compares typical all inclusive leases with standard leasing to highlight the differences:

| Cost category | All inclusive lease | Standard lease |

|---|---|---|

| Road tax | Included | Lessee pays separately |

| Maintenance & servicing | Included | Lessee arranges and pays |

| Warranty | Included | May be separate or included |

| Breakdown cover | Included | Lessee arranges separately |

| Fuel | Excluded | Excluded |

| Excess damage | Excluded | Excluded |

| Tyre wear replacement | Excluded | Excluded |

| Monthly cost | Higher but predictable | Lower but variable |

This clarity helps you decide whether the convenience and cost certainty of all inclusive leasing justify the slightly higher monthly payments compared to standard agreements.

Common misconceptions about leasing with bad credit

Several myths persist about leasing vehicles when you have poor credit, creating unnecessary barriers for people who could benefit from flexible leasing options. One widespread misconception is that all leases require hard credit checks that damage your credit score. In reality, soft checks or no checks are common among UK short-term and all inclusive providers, preserving your credit rating whilst assessing affordability. Another false belief is that bad credit automatically leads to prohibitively high deposits. Many providers now offer zero or reduced deposits, especially for shorter lease terms where risk is managed differently.

A third myth suggests that all inclusive means absolutely no extra costs. Whilst bundled services cover tax, maintenance, and breakdown assistance, you still pay for fuel and damage beyond normal wear and tear. Understanding this distinction prevents budget miscalculations. Additionally, the term "no credit check" can be misleading because providers may still verify your identity through DVLA checks or conduct soft financial assessments without impacting your credit file.

Key misconceptions debunked:

- Not all leases harm your credit score; soft checks leave no negative mark

- Bad credit doesn't always mean large deposits; many providers offer low or zero deposit options

- All inclusive covers many costs but excludes fuel and excessive damage

- "No credit check" may still involve identity verification or soft assessments

- Reading contract fine print carefully prevents unexpected penalties or charges

By separating fact from fiction, you can approach all inclusive leasing with realistic expectations and make informed decisions about your vehicle needs.

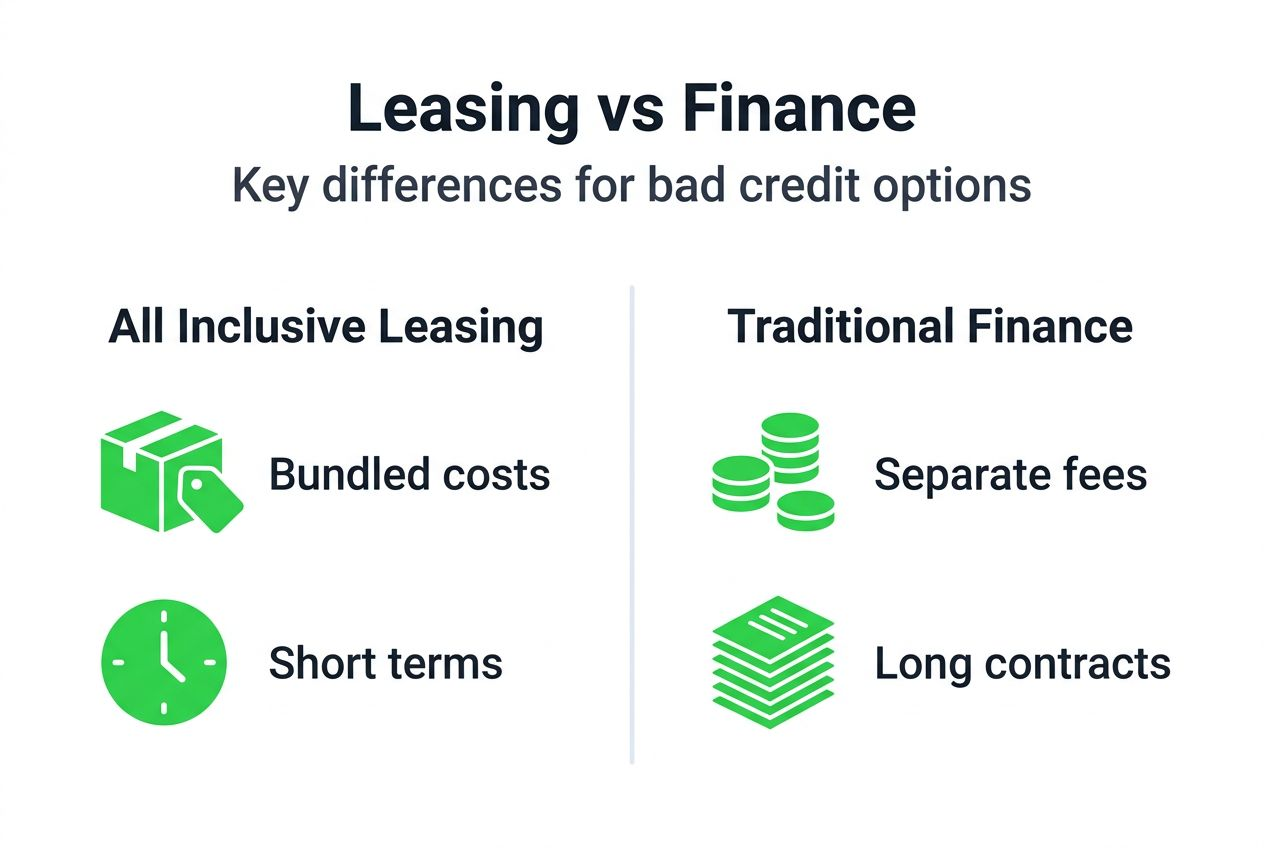

Comparison of all inclusive leasing vs traditional vehicle finance for bad credit

Choosing between all inclusive leasing and traditional finance depends on your credit situation, budget flexibility, and how long you need the vehicle. All inclusive leasing typically offers shorter contracts from 6 to 24 months, whilst traditional finance agreements like personal loans or PCP span 24 to 48 months or longer. Leasing providers use soft or no credit checks, avoiding the hard inquiries that traditional lenders perform and that can lower your credit score. This makes leasing accessible to people with poor or limited credit who might face rejection from banks or finance companies.

Monthly payments differ significantly in structure. All inclusive leasing bundles road tax, maintenance, warranty, and breakdown cover into one fixed fee, simplifying budgeting. Traditional finance separates these costs, requiring you to arrange and pay for them independently, which can lead to unpredictable expenses. Deposits are usually lower or zero for all inclusive leases, whereas traditional finance often demands substantial upfront payments to secure approval. Leasing provides flexibility to return or swap vehicles at the end of short terms, adapting to changing needs. Finance builds ownership equity but carries the risk of repossession and further credit damage if payments are missed.

The table below summarises key differences:

| Feature | All inclusive leasing | Traditional vehicle finance |

|---|---|---|

| Contract length | 6 to 24 months | 24 to 48+ months |

| Credit check type | Soft or none | Hard check |

| Monthly payment | Higher, includes bundled services | Lower, excludes services |

| Deposit | Low or zero | Often substantial |

| Flexibility | High, easy to return or swap | Low, committed until paid off |

| Ownership | Never own the vehicle | Own at end of term |

| Credit impact | Minimal or none | Potential negative if missed payments |

| Budget certainty | High, fixed costs | Variable, separate service costs |

This comparison helps you weigh the trade-offs between short-term flexibility and long-term ownership, particularly when credit challenges limit your finance options.

Practical steps to lease a car with bad credit in the UK

Securing an all inclusive lease when you have bad credit involves a straightforward process if you prepare properly. Follow these steps to improve your approval chances and get on the road quickly:

- Browse suitable vehicles and short-term contracts from providers specialising in bad credit leasing.

- Prepare essential documents including photo ID, valid UK driving licence, proof of income such as payslips or bank statements, and DVLA address confirmation.

- Submit applications to providers offering soft or no credit checks to avoid negative credit score impacts.

- Await approval, which typically takes a few days, and review explained terms carefully before signing.

- Arrange delivery or collection of your vehicle, often available shortly after approval depending on stock.

- Maintain the vehicle according to the agreement, keeping it clean and reporting any issues promptly.

- Return or renew the lease at the end of the term, choosing a different vehicle or extending if needed.

Typical timelines see approval within days of application, with delivery following shortly once documentation is verified and the vehicle is prepared. Speed depends on vehicle availability and the completeness of your paperwork.

Pro Tip: Provide clear and honest income proofs along with accurate address documentation to avoid delays and demonstrate reliability to the provider.

Before committing, compare multiple providers to identify the best terms and pricing. Read lease agreements fully, paying attention to mileage limits, early termination penalties, and damage clauses. Understanding these details upfront prevents unexpected costs and ensures the lease suits your budget and usage needs. Taking time to prepare and compare options significantly improves your leasing experience.

Benefits of all inclusive leasing for individuals and small businesses

All inclusive leasing delivers several advantages that directly address the challenges faced by people and businesses with bad or limited credit. Avoiding hard credit checks preserves your credit score, giving you a chance to rebuild without further damage. Fixed monthly payments simplify budgeting by eliminating surprise costs for maintenance, tax, or breakdowns, which is especially valuable for self-employed individuals managing fluctuating income. Flexible lease durations from 6 to 24 months suit changing personal circumstances or business demands, allowing you to scale vehicle access up or down as needed.

You gain access to newer, well-maintained vehicles without the ownership risks of depreciation or resale hassles. Bundled services reduce administrative burden and stress, freeing you to focus on work or family rather than chasing service appointments or tax renewals. Small business users particularly benefit from predictable vehicle costs that ease cash flow management and financial forecasting. Improved mobility directly influences employment opportunities and business operations, enabling you to reach clients, commute to jobs, or deliver goods reliably.

Key benefits include:

- No hard credit check impact preserves and protects your credit score

- Fixed monthly payments aid precise budgeting and reduce financial uncertainty

- Flexible lease durations suit changing personal or business needs

- Access to newer, well-maintained vehicles without ownership risks

- Bundled services reduce hassle and unexpected vehicle expenses

- Suitable for self-employed and small business users managing fluctuating income

- Improved mobility positively influences employment opportunities and business operations

These advantages make all inclusive leasing a practical, accessible solution for anyone needing reliable transport without the barriers and risks of traditional vehicle finance.

Discover flexible all inclusive car leasing options today

If you're ready to access reliable, flexible vehicle leasing without worrying about credit checks or hidden fees, flexible all inclusive car leasing options are designed for you. Flexi Auto Lease specialises in short-term leases from 6 to 24 months, using soft credit checks to approve individuals and small businesses with bad or limited credit. You'll benefit from transparent, fixed monthly payments that include road tax, maintenance, warranty, and breakdown cover, eliminating surprise costs and simplifying your budget.

Applications are straightforward and quick, with approvals often completed within days. Nationwide delivery ensures you can access quality vehicles wherever you are in the UK, supporting your mobility needs whether you're self-employed, starting a new job, or running a small business. Take the next step towards flexible, trustworthy vehicle leasing that puts you in control without compromising your credit score or financial stability.

Frequently asked questions

Can I lease a car with bad credit through an all inclusive car lease?

Yes, many UK providers offer all inclusive leases with soft or no credit checks specifically designed for bad credit applicants. You'll typically need proof of income and a valid UK driving licence to demonstrate affordability and identity.

What costs are included in an all inclusive car lease?

Road tax, maintenance, warranty, and breakdown cover are usually included in your fixed monthly payment. Fuel and damage beyond normal wear must be paid separately by you.

How long can I lease a car with bad credit?

Leases often range from 6 to 24 months, providing flexibility to suit changing circumstances. Shorter terms reduce credit risk and upfront costs for bad credit lessees.

Will an all inclusive lease affect my credit score?

Many all inclusive leases use soft or no credit checks, which do not affect your credit score. Traditional finance agreements typically involve hard checks that can negatively impact credit.