Needing a reliable vehicle when your credit history is less than perfect can feel like hitting a wall. You know you need the car or van, but the thought of being turned down puts many people off even trying. The good news is that affordable vehicle leasing in the UK is genuinely accessible for people with poor or limited credit, and the process is far more straightforward than most expect. This guide walks you through everything, from understanding your options to signing your agreement and building a stronger financial future along the way.

Table of Contents

- Understanding affordable vehicle leasing options

- What you need before applying

- Step-by-step: The affordable vehicle leasing process

- Making your lease more affordable: tips and common pitfalls

- Verifying approval and moving forward

- Get started with affordable vehicle leasing

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Specialist leases are available | Even with poor credit, you can secure a flexible vehicle lease by using the right process and providers. |

| Preparation increases approval odds | Gathering proper documents and budgeting realistically boosts your application chances and affirms affordability. |

| Step-by-step process keeps you on track | Following a clear sequence helps you avoid mistakes, save money, and secure the best terms possible. |

| On-time payments build your future | Consistently paying on time not only keeps you on the road but also improves your financial prospects. |

Understanding affordable vehicle leasing options

Before you start comparing deals, it helps to understand exactly what affordable leasing means for someone in your position. There are two main products to know about: Personal Contract Hire (PCH) and Business Contract Hire (BCH).

PCH for poor credit works by paying fixed monthly rentals plus an initial payment for use of a new vehicle, typically over two to four years, returning it at the end with no ownership option. It is the most common route for individuals. For those running a business, BCH offers VAT reclaim of between 50% and 100% depending on use, plus tax deductibility, making it well suited to sole traders and limited companies alike.

Here is a quick comparison to help you decide which suits you best:

| Feature | PCH (personal) | BCH (business) |

|---|---|---|

| Who it suits | Individuals | Sole traders, companies |

| VAT reclaim | No | Yes, 50–100% |

| Tax deductible | No | Yes |

| Ownership at end | No | No |

| Typical term | 2–4 years | 2–4 years |

You can also explore the types of vehicle leases available in the UK to find the right fit for your circumstances. Key things included in most affordable lease packages are:

- Road tax for the duration of the agreement

- Breakdown cover in many all-inclusive deals

- Fixed monthly payments for easy budgeting

- Option to add maintenance packages

- Flexible mileage allowances to suit your lifestyle

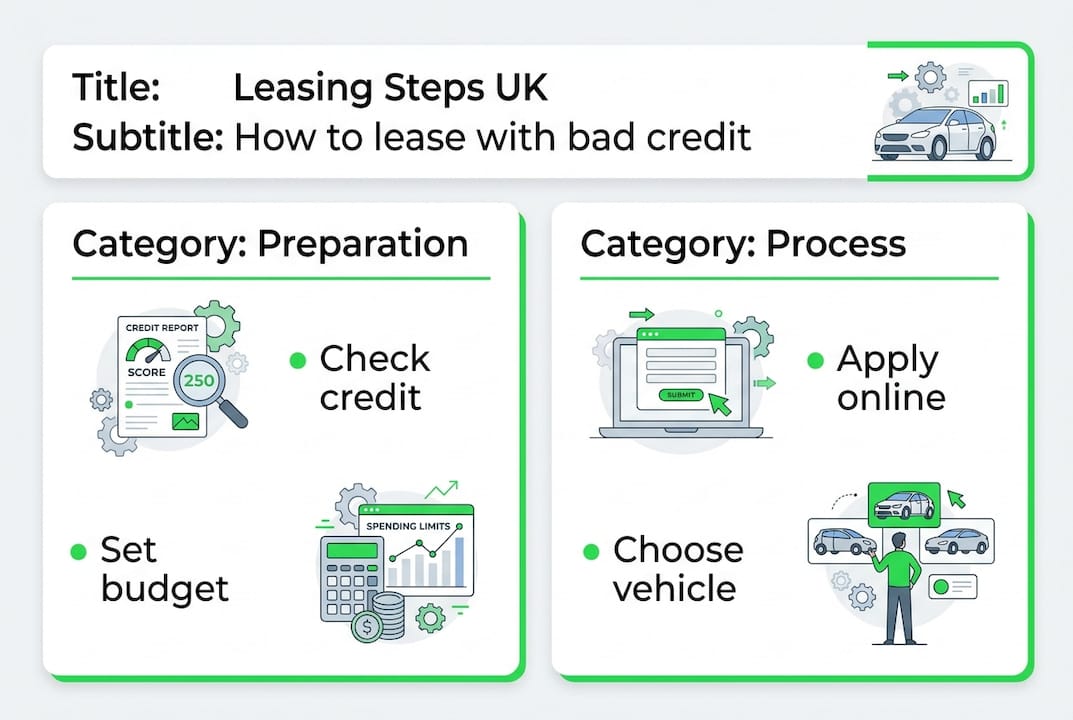

What you need before applying

Once you know which leasing route fits your situation, the next step is to gather everything needed to present a strong application. Being prepared makes a real difference, especially when your credit history is not spotless.

Most providers will ask for the following:

- Proof of identity: Passport or driving licence

- Proof of address: A recent utility bill or bank statement (within three months)

- Proof of income: Payslips, bank statements, or self-assessment tax returns if self-employed

- Bank details: For setting up your direct debit

- Employment details: Your employer's name and address, or business registration if applicable

Budgeting honestly is just as important as gathering documents. Approval strategies for bad credit include offering a larger initial payment (typically three to twelve months' rentals upfront), choosing vehicles with lower monthly costs in the £200 to £500 range, using a guarantor or co-signer, and working with specialist providers who focus on affordability rather than credit history alone.

If you are unsure where to begin, reading about leasing a car with bad credit can give you a clearer picture. You might also find it useful to understand the leasing benefits for low credit applicants specifically.

Pro Tip: Check your credit report before you apply. You can do this for free through services like Experian or Equifax. Knowing your score helps you choose the right provider and avoid unnecessary rejections that could further affect your rating.

Step-by-step: The affordable vehicle leasing process

Properly prepared, you are now ready to begin. Follow these practical steps for the smoothest experience possible.

- Compare offers. Use specialist brokers or providers who cater to poor credit profiles. Look at all-inclusive leasing options that bundle road tax and maintenance into one monthly payment.

- Submit your application. Fill in the provider's form accurately. Incomplete or inconsistent information slows things down considerably.

- Pass affordability checks. Most specialist providers focus on whether you can comfortably afford the monthly payments rather than running a hard credit search. This protects your score.

- Pay your initial rental. Once approved, you will pay the agreed upfront amount. This is usually the equivalent of three to nine months' rentals.

- Sign your agreement. Read every clause carefully before signing. Pay attention to mileage limits, excess wear charges, and early termination fees.

- Arrange collection or delivery. Many providers offer nationwide delivery, so you could be driving within days of approval.

Important: Avoid submitting multiple applications to different providers at the same time. Multiple applications can drop your credit score further, making future approvals harder. Apply to one specialist provider at a time.

If you want to understand the advantages of shorter agreements, the short-term leasing benefits for bad credit applicants are worth reviewing before you commit. You can also look at improving approval chances with a few targeted steps before you apply.

Making your lease more affordable: tips and common pitfalls

With the basic process complete, it is important to know how to get the very best deal and avoid setbacks that cost more in the long run.

Here are the most effective strategies for keeping costs down:

- Choose a practical vehicle. A smaller, lower-value car will always carry a lower monthly payment. Resist the temptation to stretch your budget for a premium model.

- Consider electric vehicles. EV leasing advantages for limited credit applicants include lower running costs and some very competitive monthly rates in 2026.

- Opt for a used vehicle lease. Flexible or short-term leasing can cost more monthly than longer agreements, but used vehicle leases often offset this with a lower base price.

- Negotiate your mileage allowance. Only pay for the miles you actually need. Overestimating wastes money; underestimating leads to costly excess mileage charges at the end.

- Add a maintenance package. Bundling servicing and tyres into your monthly payment removes surprise costs and keeps your outgoings predictable.

Pro Tip: Working with a specialist broker who focuses on poor credit profiles can save you significant time and money. They know which lenders are most likely to approve your application and can often negotiate better terms on your behalf.

Common mistakes to avoid:

- Overstretching your budget by choosing a vehicle you cannot comfortably afford

- Not reading the fine print around excess mileage and wear and tear

- Making multiple simultaneous applications and damaging your credit score further

- Ignoring the total cost of the lease, including the initial payment and any optional extras

If you are weighing up your options, comparing leasing vs hire purchase can help clarify which route makes more financial sense for you. For those needing a commercial vehicle, bad credit van leasing is also a viable and increasingly popular route.

Verifying approval and moving forward

After you complete the steps and avoid the main pitfalls, here is what happens as you move from approval toward enjoying your new vehicle.

- Approval notification. Most specialist providers respond within 24 to 48 hours. You will receive confirmation by email or phone, along with any conditions attached to your approval.

- Verification of details. The provider may ask you to confirm your identity, income, or address documents before finalising the agreement. Have these ready to speed things up.

- Final paperwork. You will receive your lease agreement to review and sign. Take your time with this step. If anything is unclear, ask before you sign.

- First payment and delivery. Your initial rental is collected, and delivery is arranged. Many providers offer a specific delivery window so you can plan accordingly.

- Ongoing payments. Set up your direct debit and make every payment on time. On-time lease payments can boost your credit score over the long term, opening doors to better finance deals in the future.

Maintaining open communication with your provider throughout the lease is equally important. If your circumstances change, speak to them early. Most specialist providers are far more flexible than traditional lenders when it comes to finding solutions. You can also explore leasing support for new employees if you have recently started a new job and are concerned about how that affects your application.

Get started with affordable vehicle leasing

If you have poor or limited credit and need a reliable vehicle, you do not have to navigate this alone. At Flexi Auto Lease, we specialise in helping people just like you find flexible, affordable lease agreements without the stress of hard credit checks or lengthy approval processes.

We offer all-inclusive pricing, nationwide delivery, and lease terms from as little as six months, so you stay in control. Whether you need a practical city car, a family SUV, an electric vehicle, or a commercial van, our team is ready to help you find the right fit. Visit our affordable vehicle leasing experts today to browse available vehicles, check your eligibility in minutes, and get personalised advice from a team that genuinely understands your situation. Getting on the road could be easier and faster than you think.

Frequently asked questions

Can I lease a car with a poor credit score in the UK?

Yes, it is possible through specialist leasing providers who use affordability checks rather than relying solely on credit history. Larger upfront payments and working with a bad credit specialist significantly improve your chances of approval.

Does leasing a vehicle improve my credit rating?

Making your lease payments on time consistently can help improve your credit score over time. On-time payments boost scores and demonstrate responsible financial behaviour to future lenders.

Are there affordable alternatives if I am not approved for leasing?

Yes. Options include used vehicle leases, electric vehicle deals with competitive rates, personal contract purchase, or hire purchase agreements. Used or EV alternatives can offer more flexibility if standard leasing is not immediately available to you.

What is the usual contract length and cost for affordable leases?

Most standard leases run for two to four years, with monthly costs of £200 to £500 being typical for affordable options. Shorter terms of six to twenty-four months are also available through specialist providers like Flexi Auto Lease.